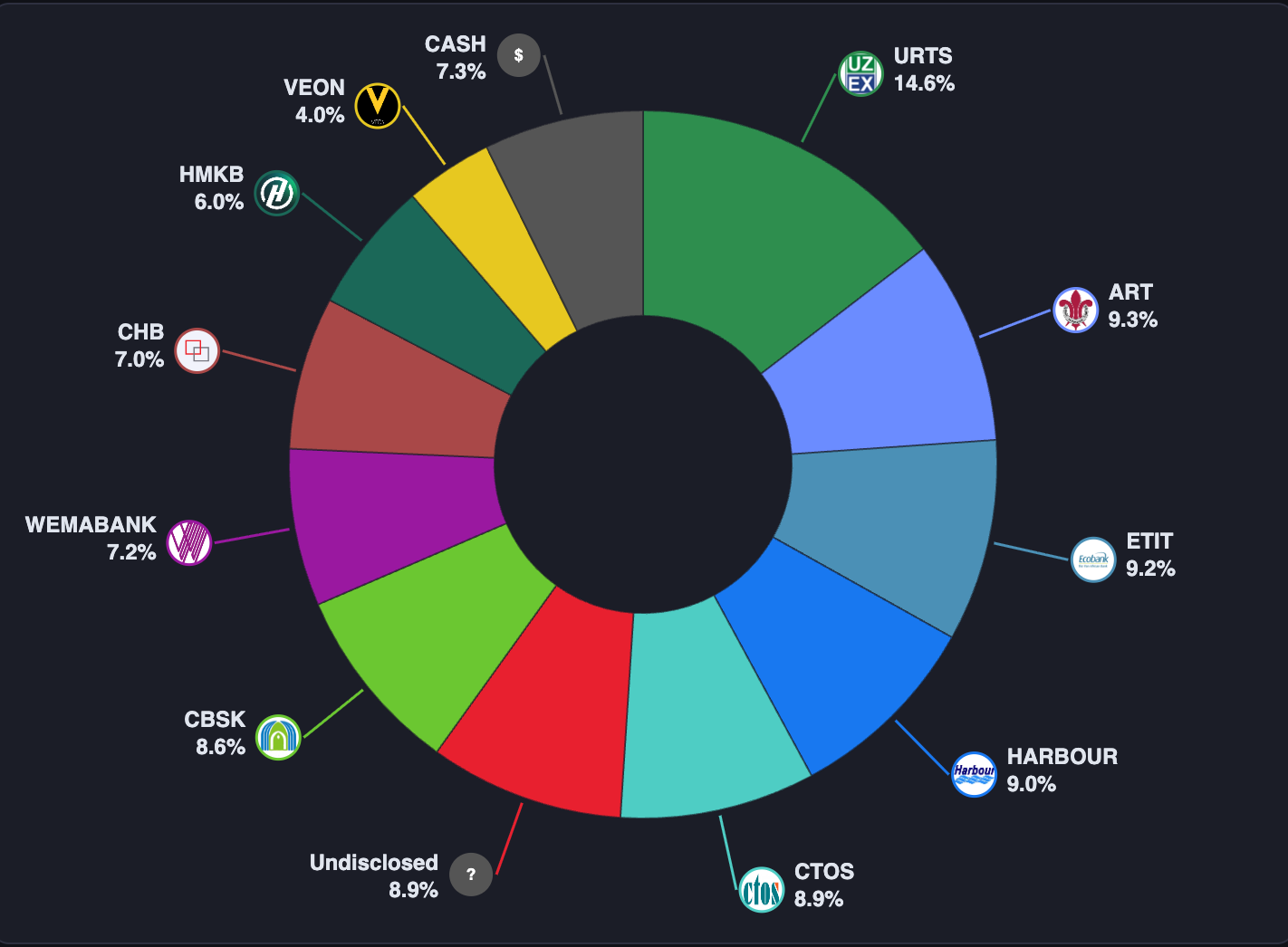

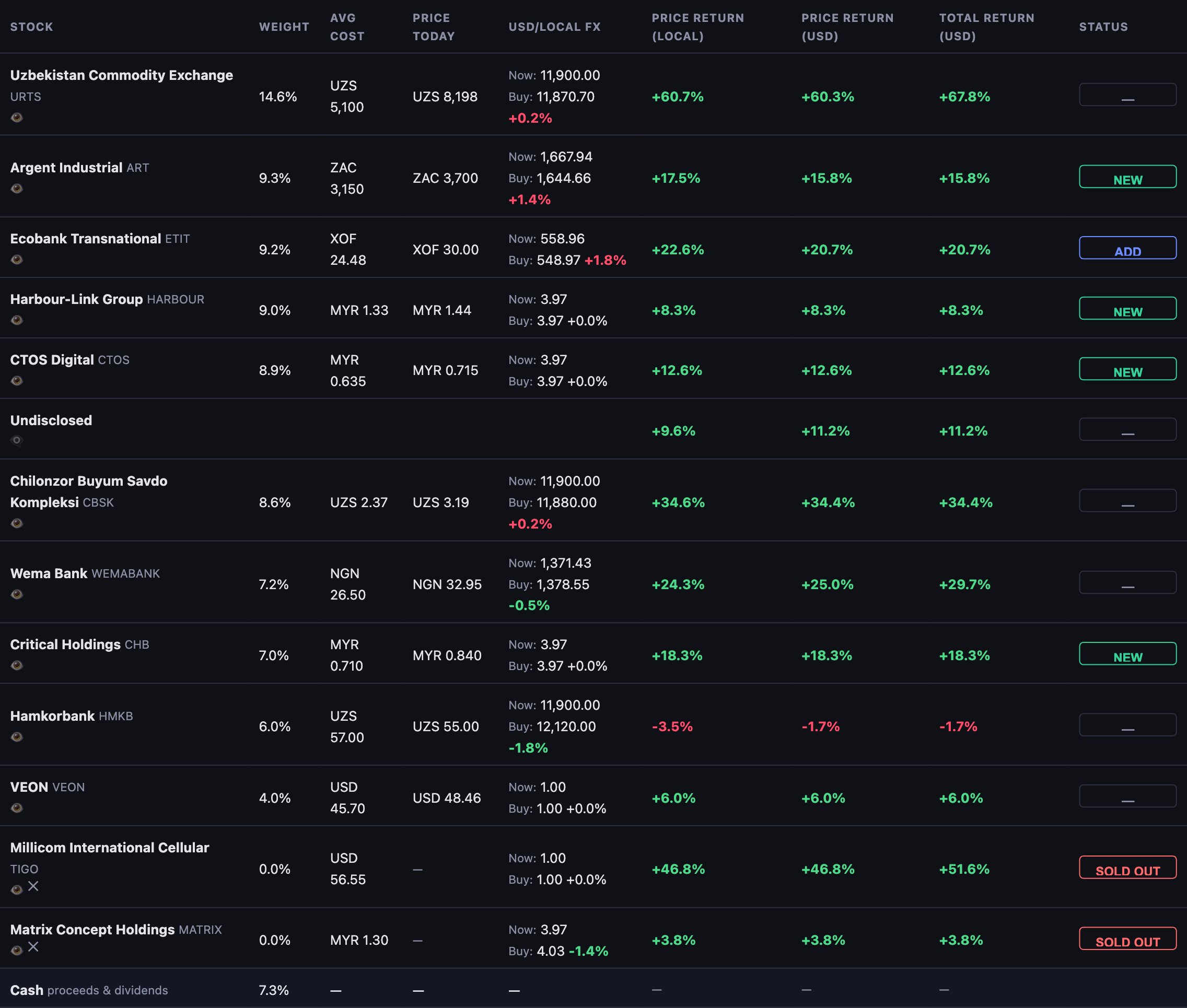

May Portfolio Update

Up 26.8% in USD terms since inception in November 2025. Eleven positions, with URTS still the largest and best performer at 14.6% weight and +60.3% USD return. The AI dashboard makes these updates very smooth to produce.

Comment on a Hold

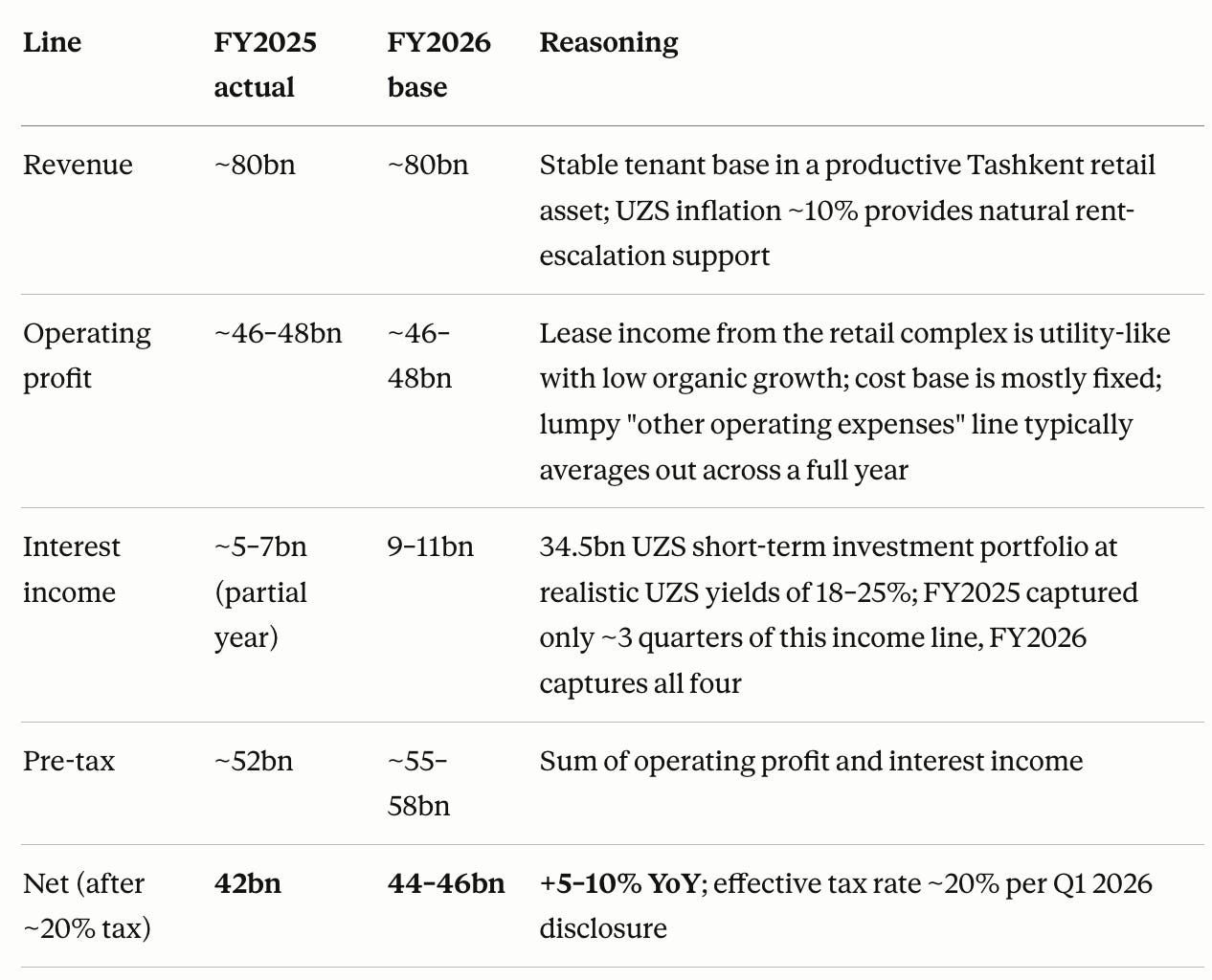

Chilonzor (CBSK) dipped a bit, but the thesis is intact. Market cap 280B UZS, no debt, 2025 net profit 42B, and they reported 2026 Q1 profit of 13B, and declared 0.2946 UZS per share dividend (~9%).

Basically the business is the same, they have just added more cash on the balance sheet that pays interest, so the growth is coming from that extra interest, not the core business. (and I think a disproportionate part of that interest came in Q1):

So even if its not growing, it’s a perfectly fine dividend paying business at 2026 forward P/E of about 6.2. And it owns 20 hectares of prime commercial real estate in central Tashkent that at current market prices is worth 3x market cap - and that’s just the land. The value of this real estate will keep going up as Uzbekistan’s economy and population keeps growing - and Uzbekistan has among the best trends of any country in the world. No idea when that will be recognised by the stock market, but I’m prepared to wait a very long time!

An additional point here is that a 9% nominal UZS yield and 6.2x forward P/E in Uzbekistan with a 14% central bank rate isn't the same as 9% dividend yield and 6x P/E in say Switzerland - most of the headline yield gets handed back through local inflation and currency depreciation.

However, Uzbekistan is doing really well macro-wise. Inflation has fallen from ~12% toward 7–8% and is heading to 5–6%, and, foreign reserves (mostly gold) have surged to a record 77B USD - over half of the Uzbek GDP which is one of the highest reserve ratios in the world. The UZS has empirically depreciated at only ~4–5% per year - and even less in 2025–2026 - rather than the ~10% the rate differential would imply, with sovereign credit upgrades further compressing the country risk premium, leaving Chilonzor with at least a defensible 4–6% USD-equivalent total return today and meaningful multiple-expansion optionality as the Uzbek central bank rate cuts eventually flow through to local discount rates.

New Positions

CTOS, Harbour-Link and Argent Industrial have been covered recently. All these are preferred holding period forever type of stocks.

Critical Holdings

The odd-man out among new positions is Critical Holdings, a Malaysian MEP engineering specialist (mechanical, electrical, process utilities). It depends on the global datacentre/semiconductor capex cycle more than the local economy. One stock like this in the portfolio is ok I’m reasoning, even if I generally like stocks that run on their local country beat, not impacted by global cycles.

The thesis for Critical Holdings is that it is founder led, 32% ROE, net cash no debt, and 24+ months of contracted backlog visibility, and increasing trend in the backlog. A resilient company that is riding the cycle, at a low price when I first wrote about it, and at a reasonable price when I bought it.

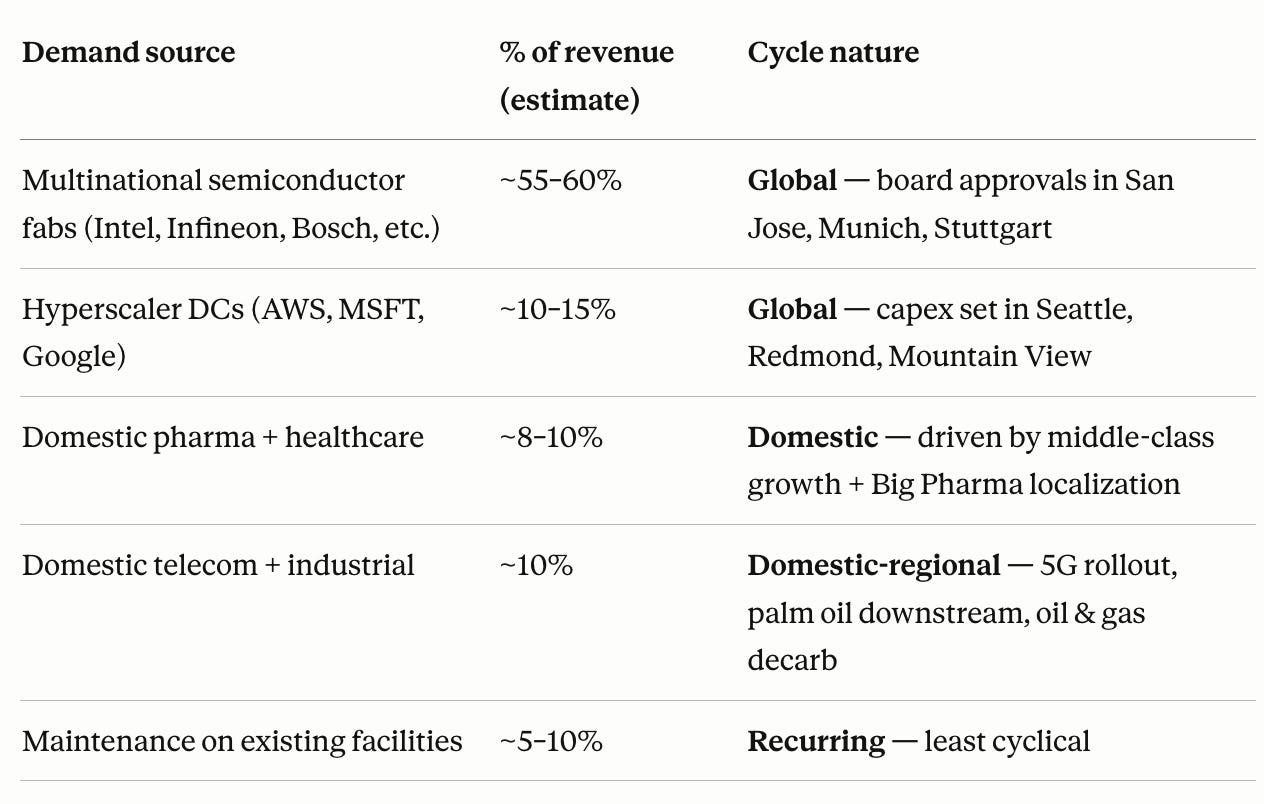

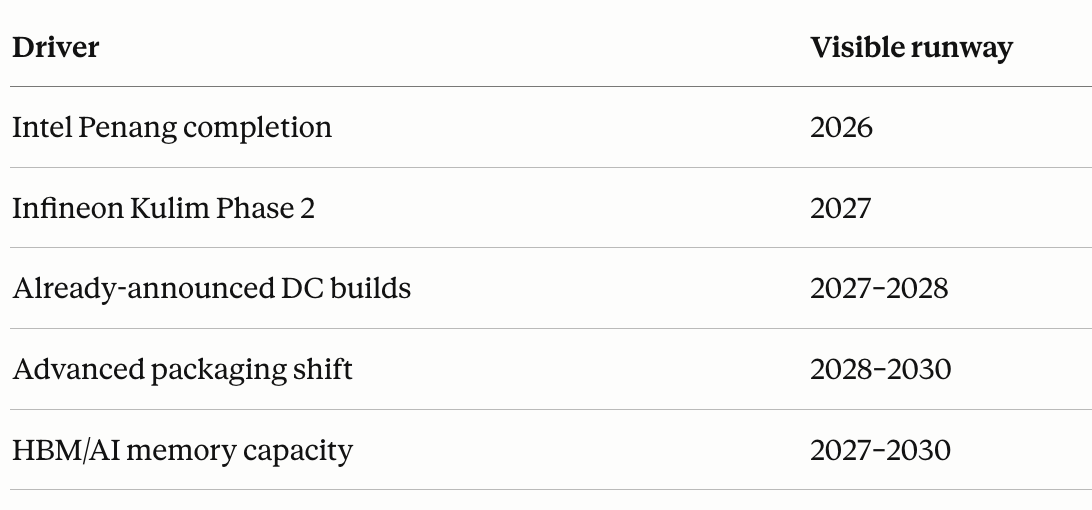

And yes it is cyclical, but the current cycle is unusually strong. It’s really two cycles overlapping: (1) Semiconductor fab capex (Intel Penang, Infineon Kulim, Bosch, advanced packaging shift from Taiwan) that started in 2022–2023. And (2) Datacenter capex (AWS Johor, MSFT, Google, ByteDance). These cycles peak in different years, which smooths the contracting backlog even if the semiconductor cycle is more important for Critical Holdings.

There is also a geopolitical driver behind it, not just cyclical. Western/ Japanese/Korean companies are doing “China+1”, i.e. a supply-chain strategy where multinationals - primarily Western, increasingly Japanese and Korean - keep their existing Chinese manufacturing footprint but build redundant or replacement capacity in a second country to reduce the China risk.

And this second country is often Malaysia for semiconductor packaging and datacenters.

So this isn’t a normal capex cycle that ends when capacity catches up to demand - it’s also a one-time relocation of supply chain that creates a 10-year or so build-out wave.

Finally, not all of Critical Holdings demand is driven by global cycles, there is also a domestic component, and a growing high margin maintenance component:

Current contracted backlog looks like this:

I think this is the key thing to watch, if Critical Holdings start to consistently not being able to replenish the backlog, it’s time to start looking to sell. At the moment though, the contracted backlog is expanding (1.15x order replenishment FY2025).

As to the impact of a potential China Taiwan conflict - a risk I think is underestimated - Xi has after all stated that a life goal of his is to re-unite China and not necessarily peacefully. In such a scenario Critical Holdings would take an initial hit as global capex pauses, but after that it could emerge as a structural winner over 18–24 months as China+1 acceleration drives unprecedented demand for Malaysian semiconductor and datacenter capacity.

Mbank

I received a very nice letter from the president of the broker in Kyrgyzstan where I opened an account, commenting on the Kyrgyzstan stocks mentioned here:

About Mbank he wrote that “The annual general meeting of shareholders was held on April 24, where Omurbek Babanov, the owner of 99% of the bank’s shares, delivered a speech. He informed shareholders about the bank’s further development and an upcoming IPO.”

This is interesting, as an issue with this stock is that the free float is very small, causing so low liquidity that it even impacts small scale retail investors. Also that I wasn’t sure how Babanov would treat minority shareholders. An IPO would alleviate both issues.

Im thinking I’ll try to buy now despite the illiquidity, and potentially benefit from a re-rating in the IPO. I’ll put this small starter position in a side pocket to the FrontierViking portfolio, as I dont have datafeeds for the Kyrgyzstan exchange.

The president ended the letter with:

“I know the “Issyk-Kul Aurora” sanatorium well and stay there annually for at least a week. I can organize your trip to Issyk-Kul at any time convenient for you.”

Sounds like I have to go to Kyrgyzstan now! Quite looking forward to checking out the place.

And in developed market retail investors don’t get personal letters from the CEO of their brokers like this. Great intangible benefit of frontier market investing!

Undisclosed

Still waiting for the person I got it from to give the go ahead to write about it publicly.

One Add

Ecobank (ETIT)

The original thesis was, it’s remarkably cheap, very profitable, but the market is spooked by lack of dividends - thinking shareholders will never see any of those profits, by Nigeria being a never ending money pit (losses and recapitalisation requirements) and by the economic crisis in Ghana. I was thinking, the problems are priced in, even if things don’t get better, they still make money and they will probably pay dividends, if not in 2026, in 2027.

So they did announce dividends in 2026, but quite low by African bank standards (2.7%), and for a little while it was seen as the worst dividend paying bank in West Africa, and the stock went down from 35 to 26.

I thought this was the BRVM equivalent of Mr Market having a panic attack about a small-but-positive piece of news. Just that they resume dividends after having payed nothing for a few years is a good signal - it means they are sufficiently capitalised to pay a dividend and are no longer blocked by regulators.

On top of that, the Nigeria business has been capitalised and is likely to swing from loss to profit in 2026 - Nigeria is one of those countries that is inflecting to the better. I’m even making currency gains on the Nigerian Naira vs the USD so far this year on Wemabank - did not see that coming! And as we have seen Ghana is not at all in a crisis any longer, and on the Ghana exchange Ecobank trades at 4x the BRVM price.

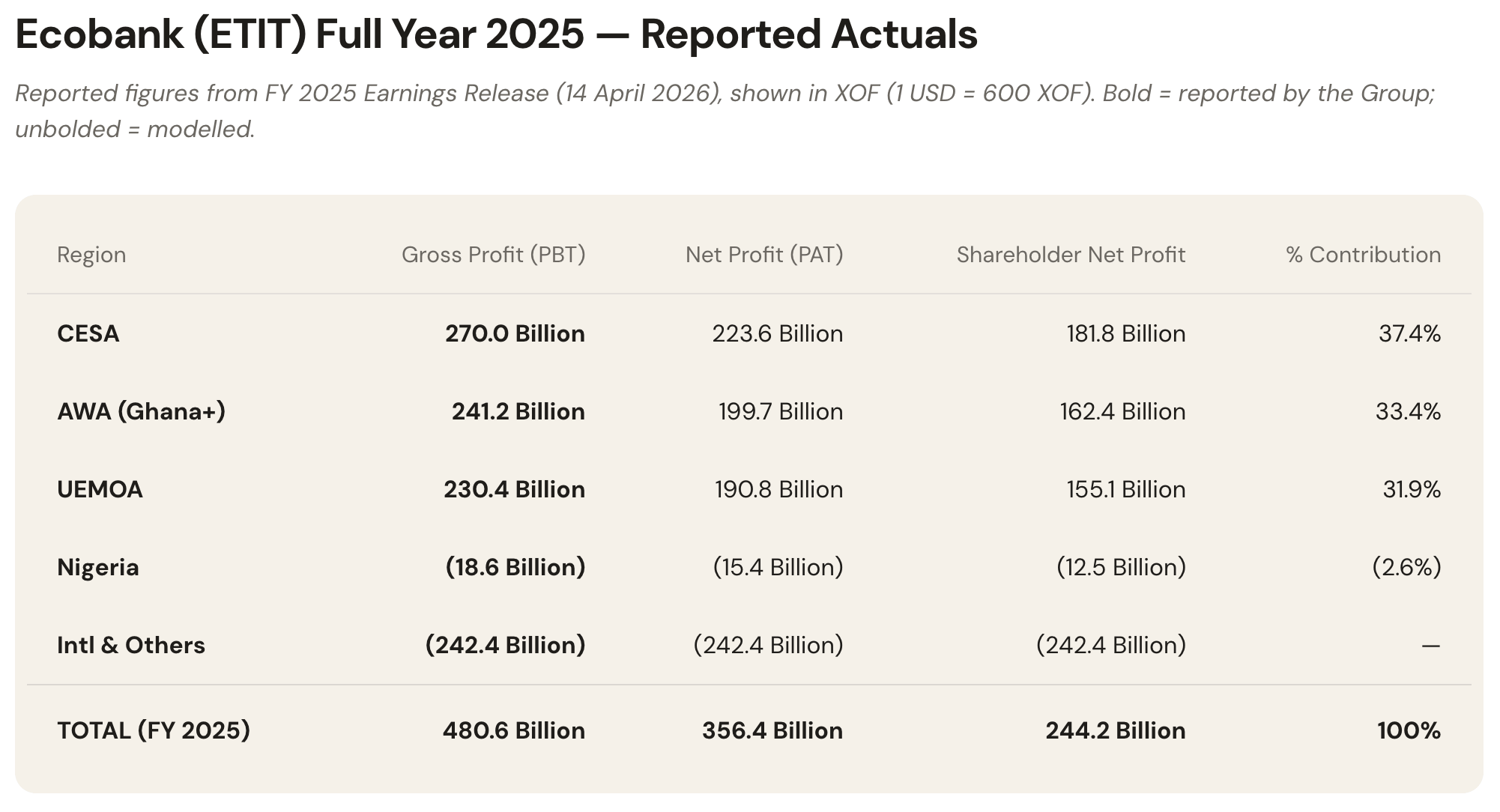

The full year 2025 results were 7% better than what I had projected (227B XOF shareholder net profit vs actual reported 244B XOF ). I’m thinking the 2026 results may well surprise to the upside from still very low expectations.

High conviction add to what probably is the lowest quality company in the portfolio. I’m still planning to sell when/if it re-rates, but I can wait 2-3 years for that.

Sells

Millicom (TIGO)

The thesis played out, the acquisition in Colombia concluded, and the stock is up 50%. Now at forward P/E 19 the risk reward isn’t as great, even if I still like the stock. Sold to redeploy in better opportunities. Got a gap in Latin America now so will check if I can find anything there. Admittedly somewhat irrational to want to cover the whole world, but you have stuff like if a China - Taiwan conflict happens, Southeast Asia will likely be hit hard, but Latin America looks a lot better.

Matrix Concepts (MATRIX)

I found other Malaysian stocks that I thought were better investments so shifted over to those instead (CTOS, Harbour Link). Matrix is a solid company and will likely do well, just a little bit less potential than the other Malaysia names. Also, I am trying to keep a concentrated portfolio, so weeding out the medium conviction names.

sad to hear tigo has to graduate out of your portfolio.

in latam there is still a large operational gap, enthusiastic and experienced backstop in core holder niel, and underperformance by distressed competition.

Very interesting portfolio - it has to be the most unique one on Substack! Great to see your holding in Argent, and I’ve started taking a closer look at your Malaysian stocks (they’re now on my watchlist).