Ghana

An error of omission

I’m realising I have completely overlooked Ghana, by far the biggest mistake of omission in the short history of this substack. Yet, the Ghanaian border is only a 3 hour drive away from where I’m usually based in the Ivory Coast.

I had written it off as a perennially fiscally irresponsible place with high interest rates and a fast weakening currency with regular IMF bailouts.

In late 2024, there was a power shift when John Mahama won the elections. Mahama’s first term in 2012-2017 was marked by economic crisis culminating in IMF bailout. Public sector wage bill grew to 70% of total budget, real GDP collapsed from 7.3% to 2.2%, the currency lost 40% of its value, debt-to-GDP shot up - the usual stuff for a mismanaged African country.

The previous administration from 2017 to 2024 under Nana Akufo-Addo did the same thing - economic crisis culminating in IMF bailout. Even topped the previous crisis on very metric: inflation peaked at 54%, the currency lost 75% of its value, and Ghana declared sovereign default in December 2022.

So when Mahama came back to power I wasn’t really paying much attention or expecting anything to change.

Mahama actually explicitly campaigned on having learned. His 2024 manifesto committed to a Fiscal Responsibility Act, an Independent Fiscal Council, and external reserve buffers. But I mean, how much do you trust politicians’ campaign promises?

Yet, the bastard went and delivered.

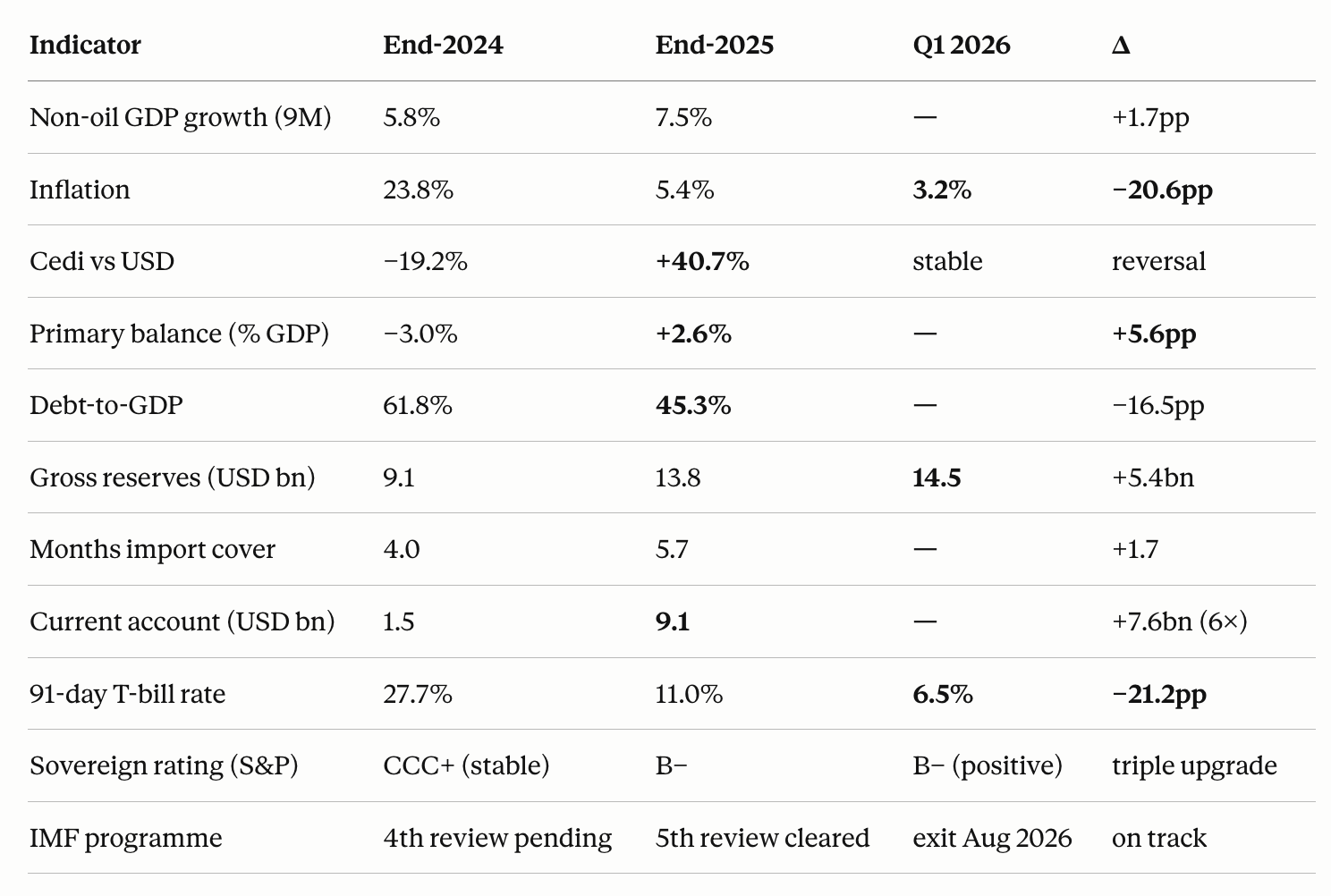

Look at these numbers:

Speaking in January 2026, Mahama said: "We shall not ease the current fiscal discipline and efficient management of the economy even in the election year of 2028."

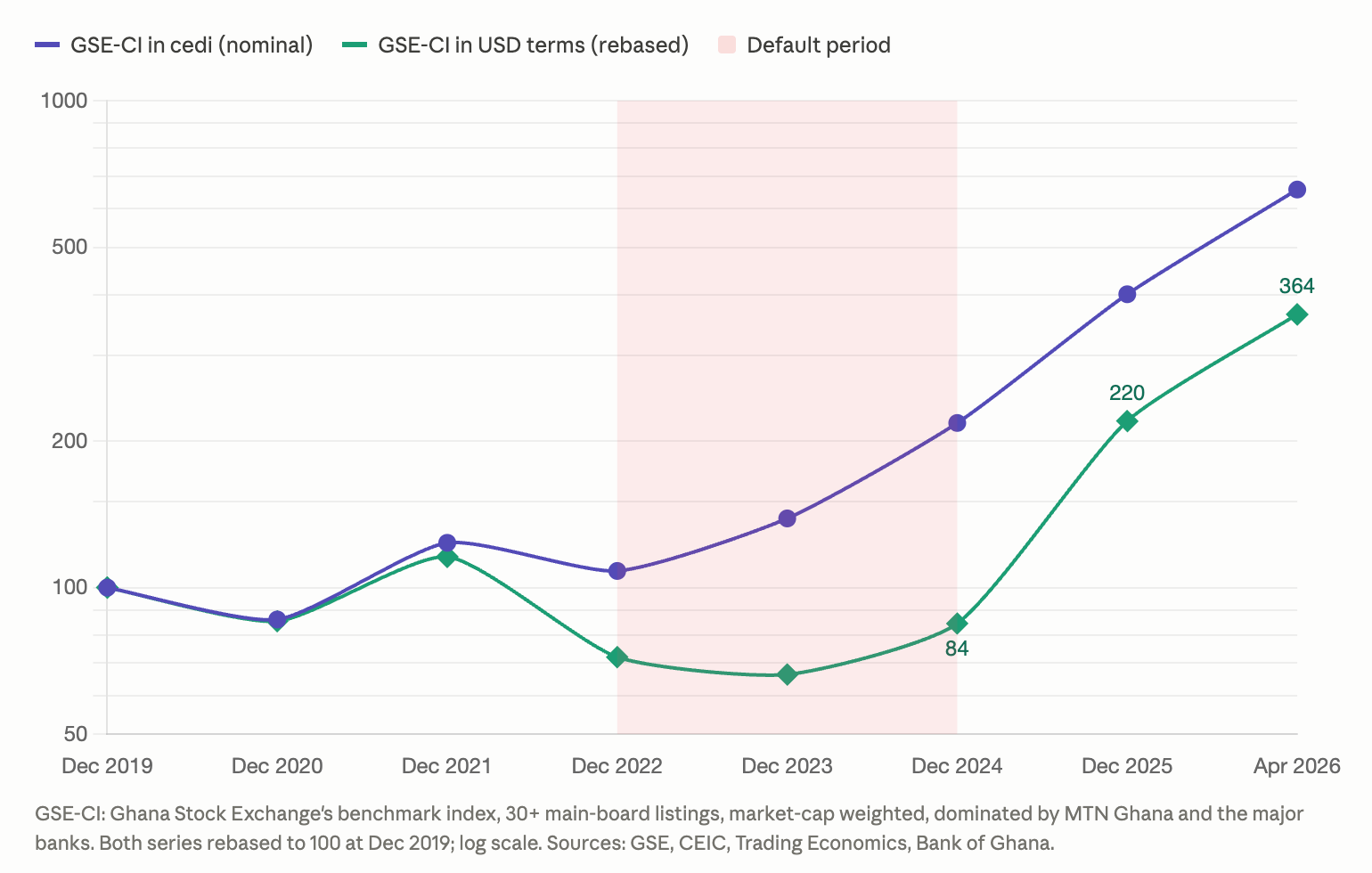

And unlike me, the Ghana stock market noticed.

So, in USD terms the whole Ghana Stock Exchange Index has done 4.3x from December 2024 to end of April 2026. Ha!

Ok, the FrontierViking portfolio includes Ecobank which is listed in Ghana, and is the second largest stock on the Ghana exchange - so Im not completely out of Ghana. Weirdly the Ghana listing of Ecobank has dislocated from the other two listings (BRVM and Nigeria) and independently followed the Ghana stock market rally.

Apparently effective arbitrage is near-impossible: shorting is banned in Ghana, transfer mechanics are brutal (takes like 8 weeks of lock up to transfer a deposit from an exchange to another if at all possible), and currency conversion plus tax friction would eat most of the spread anyway.

The BRVM-listed Ecobank even dropped recently when declaring a dividend of 0.0016 USD (about 3.4%), because the market considered that a low dividend relative to other banks. I thought that was irrational and bought a bit more.

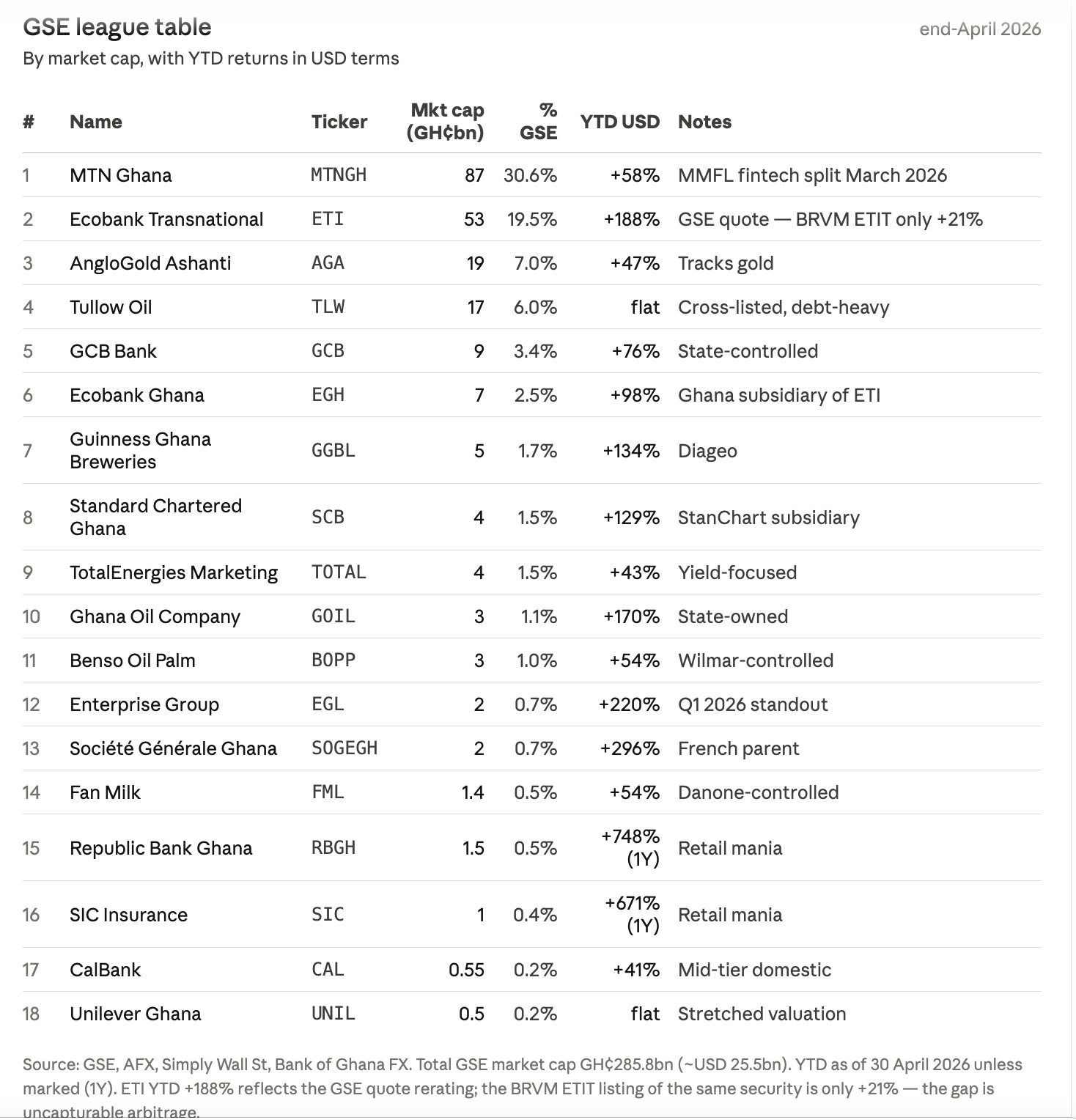

Back to the performance of Ghana stocks, here are the YTD in USD per company:

The index P/E is now up to 10.9. The deep value window is closed, but could there still be opportunities in Ghana?

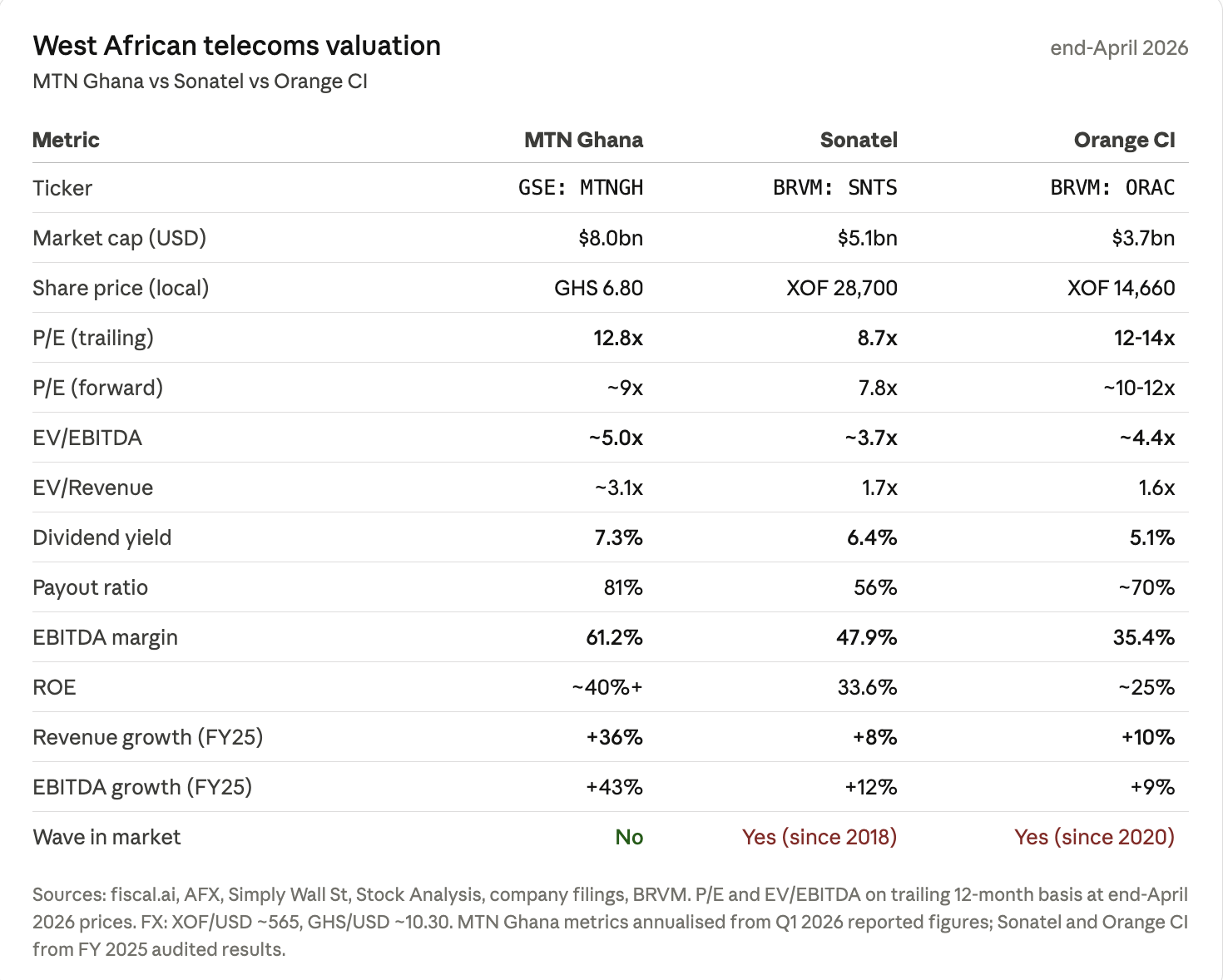

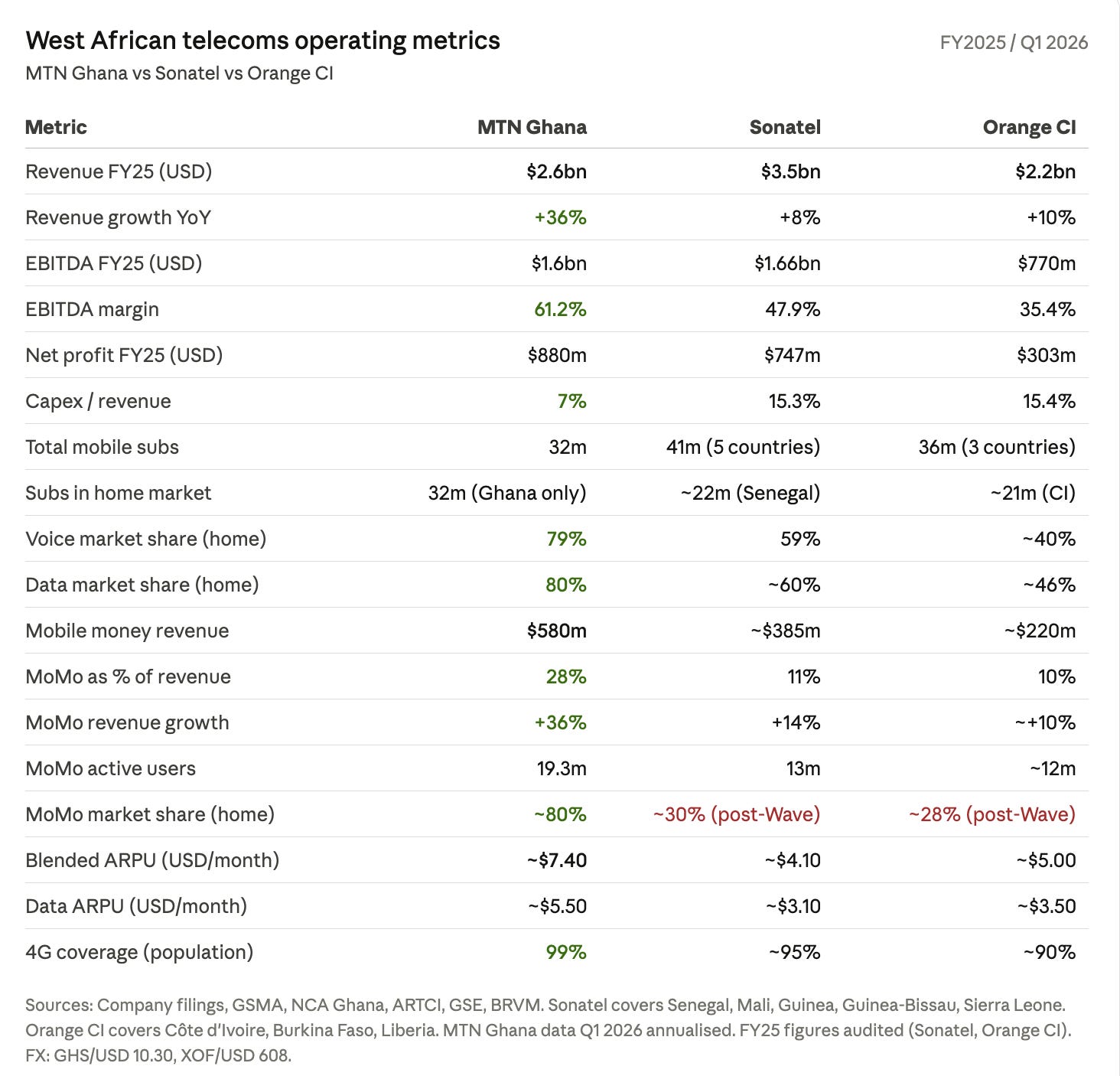

Let’s start with MTN Ghana which is a genuinely good business. High margins, high return on well everything, growing at 36% YoY. P/E 13 though, so no deep value. The thing is that MTN Ghana dominates the mobile money market in Ghana and can charge hefty fees. There is no Wave or other similar competition in Ghana. That may change though - that’s the main risk, but the whole licensing process is very slow and something one can keep track of.

Obviously would have been better to buy MTN Ghana in Dec 2024, but I think it still has some runway from today, with the ongoing impact of improved macro situation, plus the fintech spinoff catalyst (mobile money business carved out, expected Ghana Stock market listing 2028-2030). Definitely interesting.

Comparison with the two West African telecom operators on my watchlist:

Both look good. MTN Ghana wins on growth and market dominance, whereas Sonatel wins on cheapness. I'd take MTN Ghana over Sonatel today - the post-Wave reality at Sonatel doesn't justify the discount versus what MTN Ghana is doing on margins, growth, and the pending fintech catalyst. The issue is just that the FrontierViking portfolio is filling up, and there may be better opportunities elsewhere in the world.

As to other stocks in Ghana, I’m not really finding anything. Some oil companies, some banks that are meh, and lots of obviously overvalued companies that don’t compensate for the frontier market risk:

I think MTN Ghana has a lot of institutional capital so it’s sanely priced. The smaller caps on the other hand are in an euphoria stage right now, not sanely priced at all, but in the wrong direction. The opportunity was when the smaller caps were irrationally cheap, just when one could see the macro getting better.

Opportunities like Ghana in December 2024 are scattered across the world all the time. That's the thing about frontier markets - there's always a country inflecting somewhere while no one is paying attention. Missing Ghana stings, but the next one is out there. The fun is staying curious enough to find it.