Harbour-Link

Too small, too far, too boring - priced accordingly

Next up, another Malaysian business uncovered in the bubble chart.

Harbour-Link (Market Cap: 135M USD / 535M MYR)

Harbour-Link owns and operates the dominant logistics infrastructure network on the East, Borneo side of Malaysia, and also runs shipping within Malaysia and across Asia. On water the company owns a fleet of around twelve container vessels and a fleet of tugboats and barges.

On land, the company owns a network of trucks, trailers, prime movers, forklifts, cranes and heavy transport equipment, plus warehouses and cargo yards in Kuching, Bintulu, Labuan and other East Malaysian ports. It also has an engineering arm that builds petroleum storage tanks, marine terminals and piping systems, a machinery trading business that sells and rents heavy equipment to the construction and industrial sectors, and a small property development division.

In practice, this means that when a cargo ship arrives at Bintulu port carrying industrial equipment for a petrochemical plant, building materials for a data centre, or consumer goods for Sarawak’s growing middle class, Harbour-Link can handle every step of the journey: the vessel itself may be a Harbour-Link ship; the crew unloading it may work for Harbour-Link; the trucks taking the cargo to its destination are Harbour-Link trucks; and the warehouse storing it until delivery is a Harbour-Link warehouse. No other single company in East Malaysia offers this end-to-end capability across all modes.

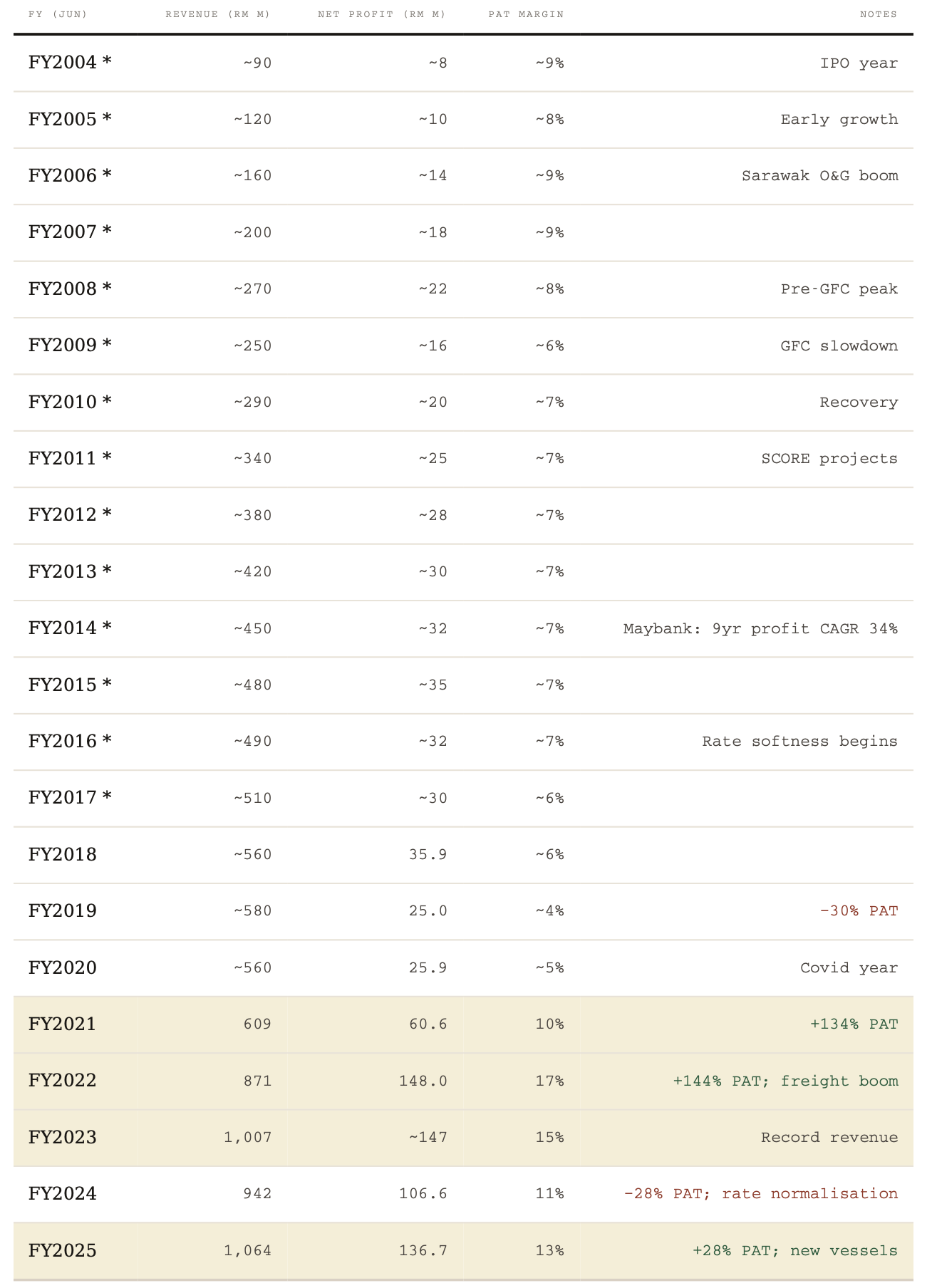

Harbour Link is a founder led company started 50 years ago, and has carefully and conservatively built up this strong position over those 50 years. It’s been profitable every year since the IPO in 2004, through shipping cycles, global financial cycles, covid and everything. It is to some extent a toll bridge on logistics in East Malaysia.

Since it has such a strong position, and operates in a capital expenditure heavy sector, one would expect a high multiple and high debt load. But ha, and this is why I love founder-led Malaysian small caps, it has P/E 4.6 , P/FCF 6.4 on FY2025 earnings, and a net cash position of 100M USD (399M MYR), i.e. 74% of it’s market cap is net cash on the balance sheet, EV/EBITDA 1.5, and a dividend yield of 5.9%.

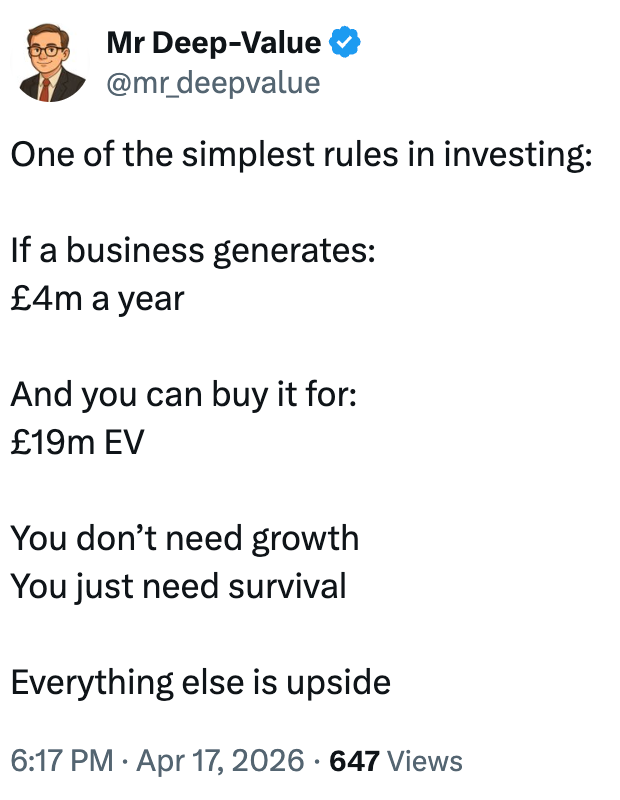

So if one adds the net cash plus 2025’s net profit after tax of 137M MYR one gets a higher figure (536M MYR) than the whole market cap (535M). So putting aside minority interests in subsidiaries (146M MYR), one could buy the whole thing for net cash and one' year’s net profit (2025 was a great year for Harbour Link admittedly, but still). The situation reminds me of this recent tweet by substacker Mr. Deep Value

For Harbour Link one has 271M MYR in EV (market cap - net cash + minority interests), and say 100M MYR generated per year. And the company is most certainly surviving.

Why Is It So Cheap?

So, we get to the usual, why is it so cheap question. Attempted answers:

It is not in a developed market, it has no analyst coverage, it is illiquid by institutional standards, and the geographic distance from Kuala Lumpur keeps it

off the radar of even the Malaysian research community.

A not insignificant portion of earnings depend on global shipping rates which move in cycles, and shipping generally has low multiples.

The global orderbook for ships in the smaller classes relevant for Harbour-Link is at its highest ratio to active fleet since 2010. Approximately 300 vessels of up to 5,000 TEU were ordered in 2025, with Chinese yards fully booked through 2028–2029. This supply wave is scheduled to hit the intra-Asia market in 2027–2028. If demand growth does not absorb the new tonnage, intra-Asia rates will come under meaningful pressure, which could affect Harbour-Link’s regional liner revenues.

I’m totally fine with the first reason. Let’s address the other two, and start with the 2024 and 2025 earnings:

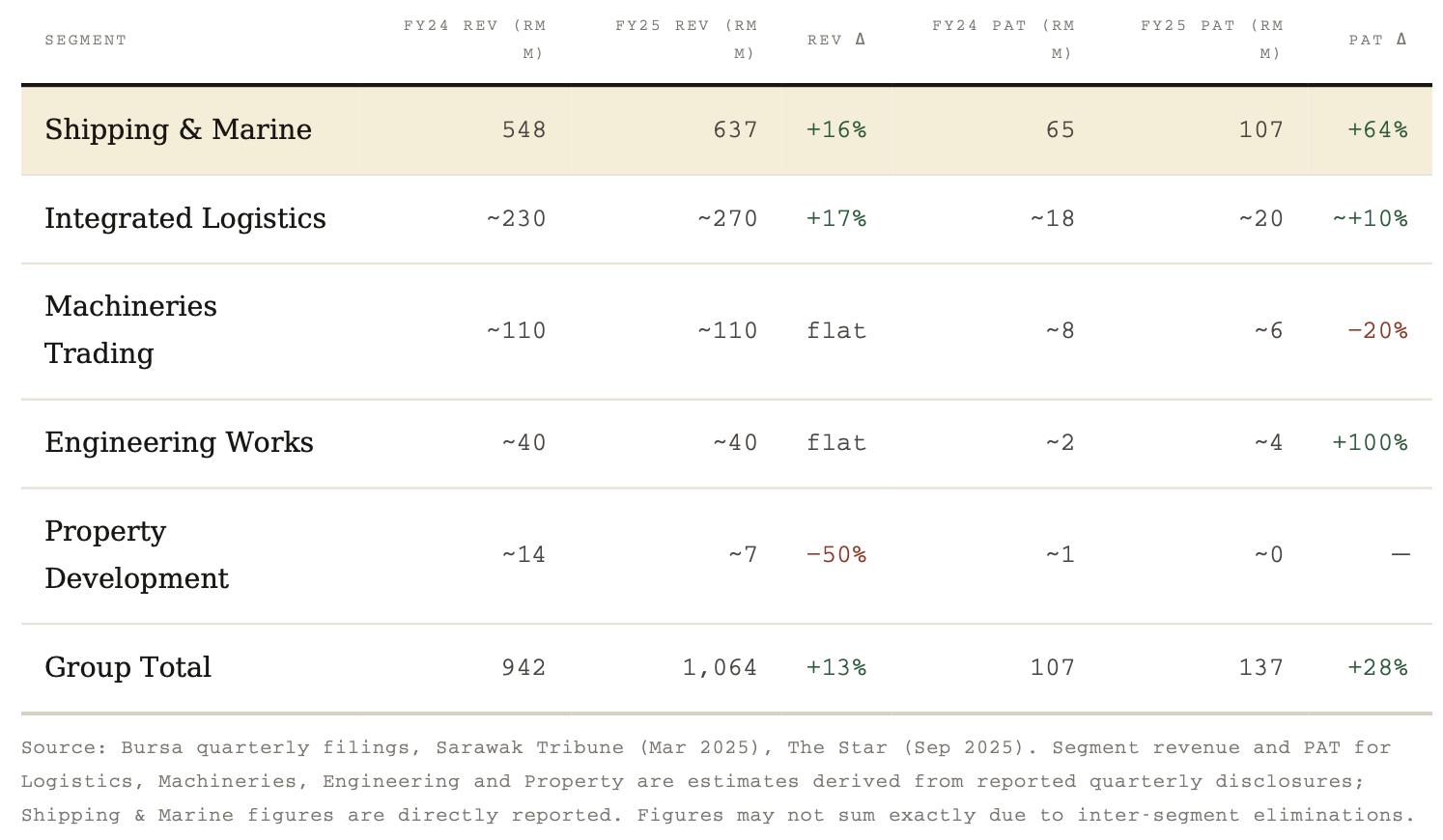

So for 2025, 107M out of 137M in PAT (Profit After Tax) came from “Shipping & Marine”. A lot - is this more a shipping company than a port and logistics operator? Well, a rough decomposition of the 2025 Shipping & Marine 107M segment, based on fleet economics and management commentary across several quarterly reports, gives:

Tugboat and barge operations: likely RM 55–65M profit - the highest-margin sub-segment

Container liner service: likely RM 35–45M profit - high revenue, lower margin

Ship agency + ship management: likely RM 5–10M combined - fee income, low capital intensity

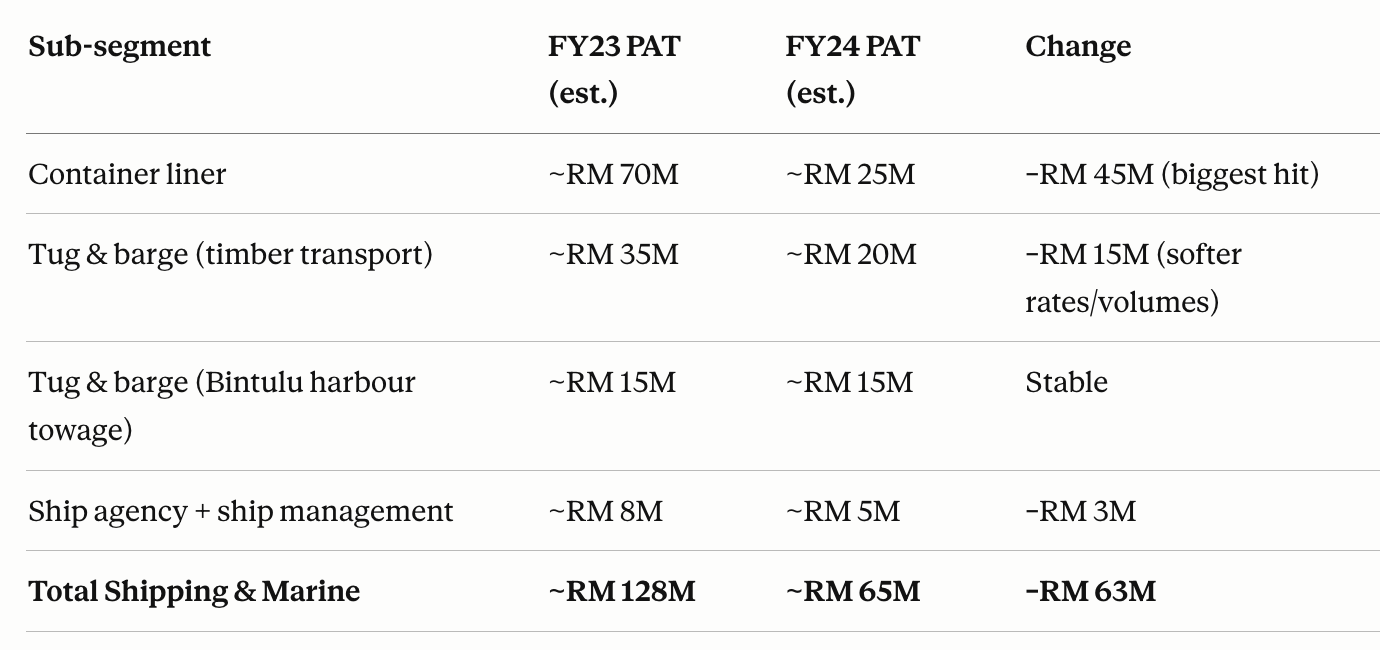

Tugboat and barge operations should be less impacted by global freight rates. Yet 2024 was a down-year in terms of freight rates, and profit went down to 65M, as if container liner went to zero. Digging into it, it turns out barges are used for harbour operations, but also for long distance shipping of timber which is impacted by freight rates. Here is an estimated breakdown of the drop from 2023 to 2024:

So in conclusion, they are impacted by freight rates, but even in a down year, Harbour-Link makes good profits, and has plenty of operations that are not freight rate dependent including all the land logistics and harbour tug and barge operations.

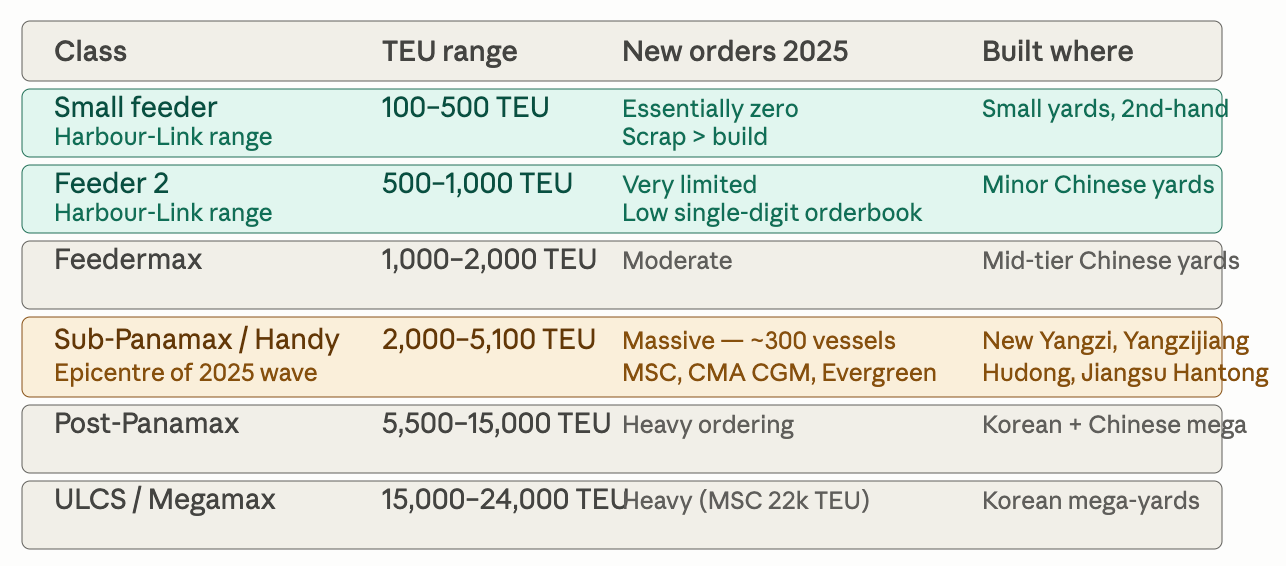

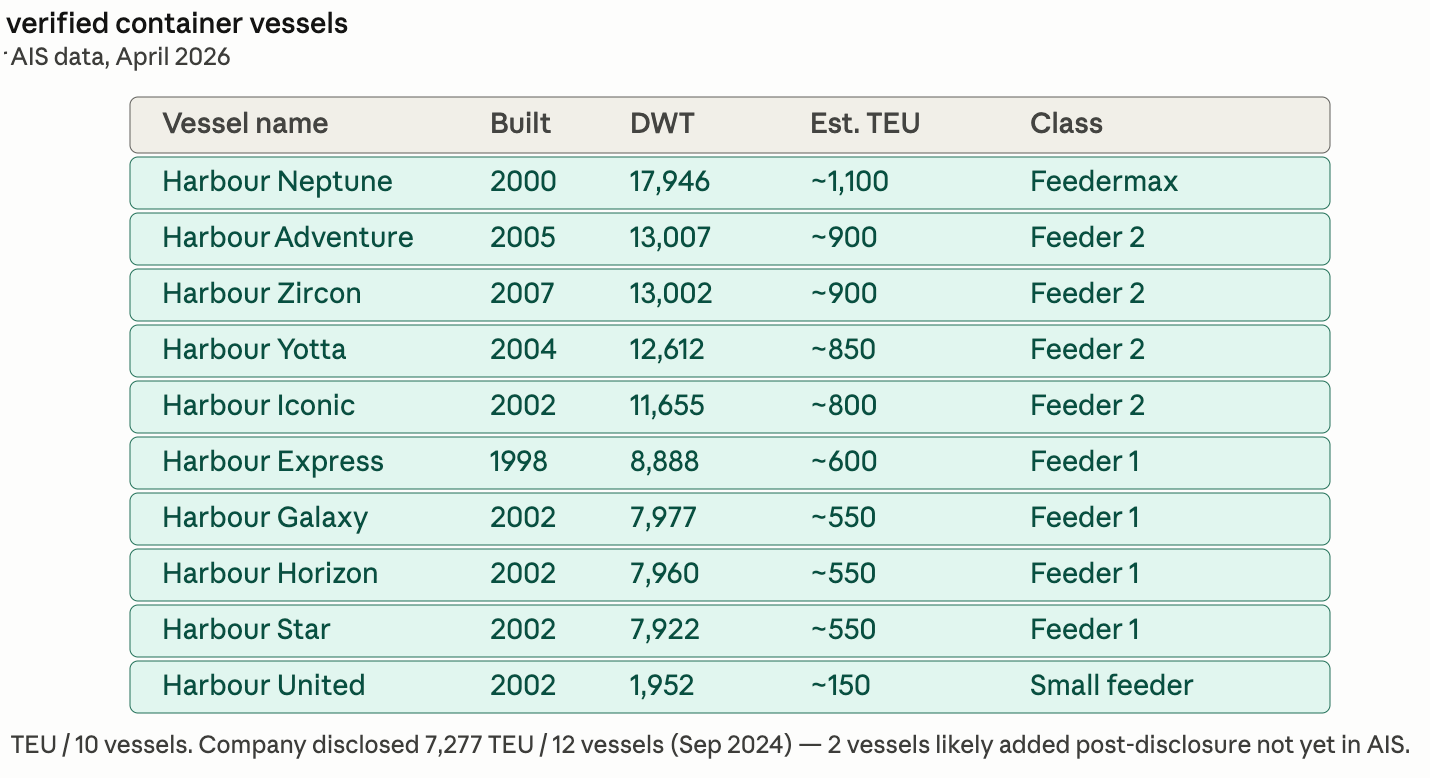

As to the Chinese shipyards running at full capacity and flooding the market in 2027-2028. It turns out Chinese shipyards are focused on the sub-Panamax/Feedermax 1,000-5,100 TEU (Twenty Foot Equivalent Unit) sizes, whereas Harbour Link’s fleet is in the smaller below 1,000 Coastal Feeder vessel size.

Harbour Link’s fleet:

All right, so Harbour Link isn’t directly impacted by a supply surge from Chinese yards, only possibly by cascading down effects, that bigger ships are used on smaller routes. However, Harbour-Link is insulated form this by Malaysian cabotage regulation, captive industrial demand, and by vessel size incompatibility with Sarawak ports - such large ships simply can’t use the ports.

The FY2024 rate pressure that did hit Harbour-Link came from a different source — it was Malaysian and regional liner operators competing more aggressively on domestic cabotage routes, not global newbuilds cascading down. This eased in 2025 for multiple reasons; Malaysians cabotage protections re-instated, some operators were unprofitable and stopped, red sea blockade pushing freight rates higher, domestic rates stabilising.

The Future

Now looking at the future, we know that Harbour-Link has made a few investments that will impact 2026 and future years, plus other infrastructure developments will benefit Harbour-Link:

2 new container vessels purchased for 100M MYR

2 new quay cranes purchased to Kuching Port Authority's Senari Terminal Two

Senari RoRo terminal - operational from August 2025. This is developed by Kuching Port Authority, but Harbour-Link benefits from the volume throughput (ship agency, stevedoring, potentially integrated logistics for vehicle distribution).

Sarawak infrastructure tailwinds - Sejingkat-Samarahan Bridge construction, Serian-Gedong dual carriageway, Public Works Department HQ construction, Data centre construction cycle in Sarawak - all require project cargo logistics and heavy haulage services that Integrated Logistics segment benefits from.

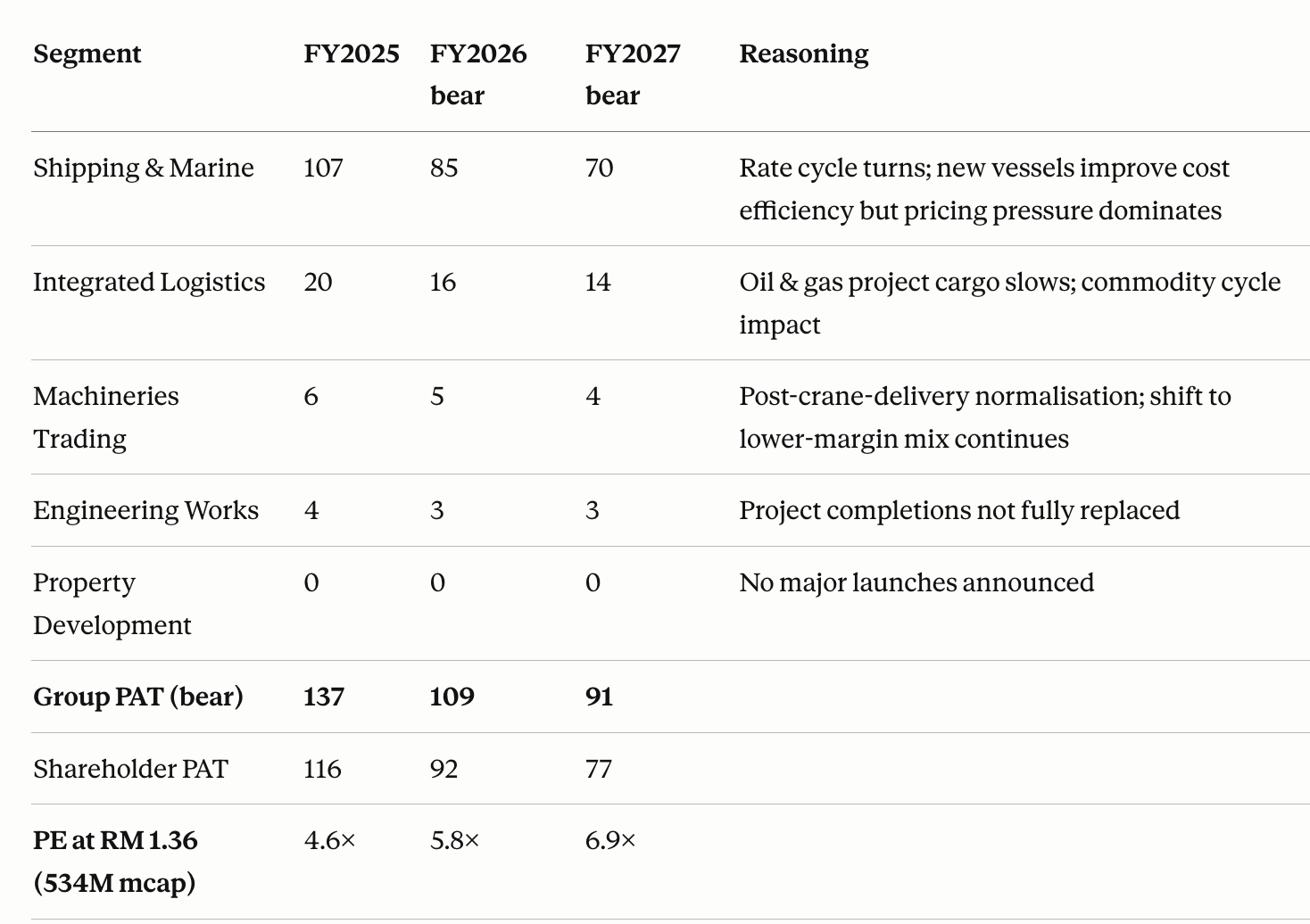

Harbour-Link hasn’t issued any guidance, but Ill do bear and bull cases. In the bear case, Im assuming Red Sea traffic resumes, and Hormuz strait goes back to normal removing global rate tailwind. Feeder cascade begins reaching intra-Asia trunk routes by late 2026. Sarawak cabotage licensing remains in place but licenses are issued liberally. Sarawak timber export volumes soften. Commodity downturn hits integrated logistics oil & gas projects.

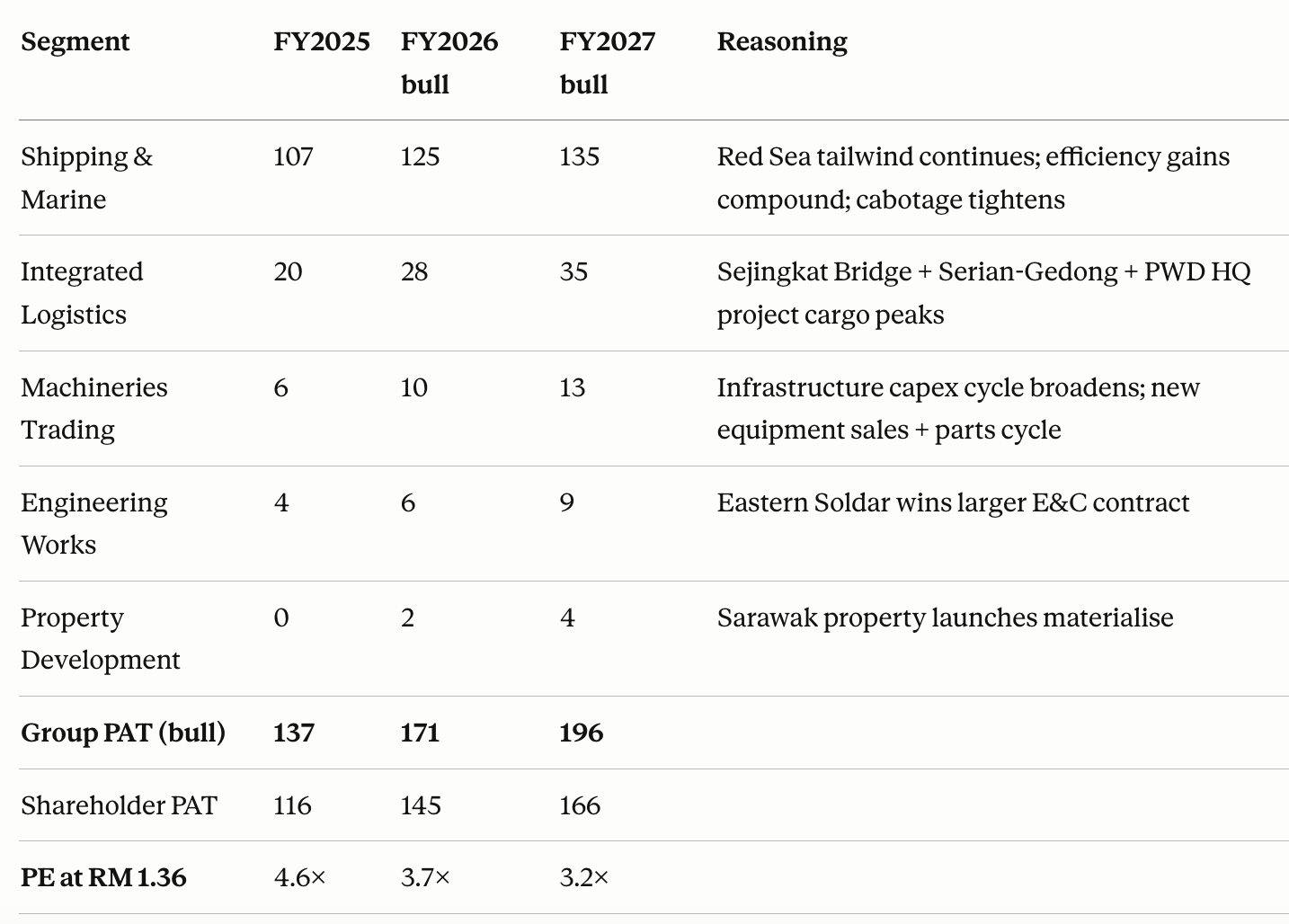

For the bull case, I’m assuming global shipping disruption continues through 2026. Cabotage protection tightens via stricter license issuance. New vessels deliver efficiency + enable additional routes. Sarawak infrastructure boom accelerates — project cargo tailwinds significant. Machinery trading benefits from infrastructure capex across Sarawak. Property launches land.

In conclusion, even in the bear case, it looks inexpensive. One thing to keep in mind though, is that it’s a capital heavy business that needs to do maintenance capex just to stay in business, so free cashflow is lower than earnings. Official free cashflow figures for 2025 (using fiscal.ai definition) were 83.3M, giving a Price/FCF multiple of 6.4 and a cash adjusted P/FCF of 1.6.

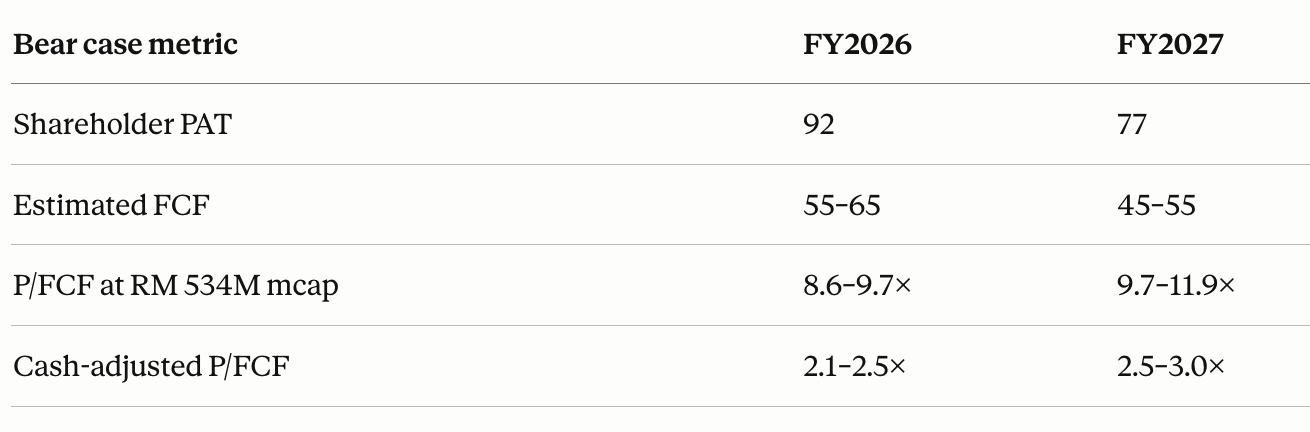

In the bear case P/FCF looks as follows:

Cash-adjusted P/FCF is still under 3 even in the bear case, impressive!

Why Is It So Cheap!!??

So after all this, Im still not sure why it is so cheap. Underestimation of the maintenance capex maybe, the fleet is quite old after all. Succession risk? Or that it is not a steady compounder, with very lumpy moves. Here are the last 20 years data:

Ok, it’s not straight up, but still very solid, always profitable, with step up moves after investments. This history actually looks founder led.

The People Behind Harbour-Link

The company was founded in Bintulu in 1975 by two men: Datuk Francis Yong Piaw Soon and Wong Siong Seh. Yong started his working life in timber export in East Malaysia in the early 1970s and pivoted into freight forwarding and shipping in 1975.

Fifty years later, he is still running the company. As of the FY2024 annual report, Yong holds the title of Chairman and Group Managing Director - both roles simultaneously, which tells you something about the concentration of authority. He is approximately 75 years old. Wong Siong Seh remains on the board as Executive Director. Together, their direct shareholdings are around 9.95% for Yong and 5.56% for Wong, with combined effective stakes considerably higher through holding vehicles.

Yong has spent five decades building this business in a city - Bintulu - that most Malaysian investors have never visited. He received the Sarawak Outstanding Entrepreneurship Award. He attends every board meeting. The 100M MYR decision to commission two new container vessels in FY2025 was not made by a professional manager with a three-year contract and equity compensation. It was made by a seventy-five-year-old man who has lived through every shipping cycle since 1975 and believes there are years of growth ahead in the market he has served his entire career.

The capital allocation record reflects this orientation. Harbour-Link has grown its fleet through internally funded capex without dilutive equity issuances or leverage-driven acquisitions. The dividend payout, while modest relative to earnings, has been consistent - and the latest at 5.9% is pretty good. This is not a cash hoarding dead-money situation. There are no obvious red flags in the related-party transaction disclosures. For a family-controlled Malaysian business, this is a clean governance record.

Verdict

The more I write and research this company the better it looks. Usually it’s the other way round, it looks great initially, and then one finds more and more issues. Really does look like an undiscovered gem. Just wish the founder was younger. But hey, Charlie Munger was sharp until the very end and went to a board meeting the week he passed away at age 99.

Harbour-Link goes into the FrontierViking portfolio.

Hey, man.. I am a new reader. Since you cover frontier/emerging markets, you should always say how/where to buy the stock. For instance, this one interested me a lot. Thanks!!

it seems that the company in the photo you used "Harbour link container service" is not a part of the listed company. I used it to search in the annual report and checked the sub list.