June Portfolio Update

Up 28.6% in USD terms since inception at the end of November 2025.

The 28.6% is the current USD value of the portfolio divided by the net USD I've actually put in - in other words, what my own dollars have earned. Turns out that's a money-weighted return, and professional managers usually pair it with a second number: the Time-Weighted Return (TWR).

TWR answers the question: “What did one dollar earn if it was invested at the start and just left alone?” by chain-linking each month's return and ignoring how much money was in the account at any moment. And here it tells a very different story: I started with just two Uzbekistan names that did really well while the portfolio was still tiny, and only added most of my capital later - so TWR weights that early run far more heavily than my wallet ever did. The TWR since inception comes out at a whopping +84%. Had to check it, because it didn’t seem right:

Dec 2025 +20.0%

Jan 2026 +13.8%

Feb 2026 +9.3%

Mar 2026 +3.9%

Apr 2026 +10.1%

May 2026 +2.8%

Jun 2026 +5.0%

─────────────────

1.20 × 1.138 × 1.093 × 1.039 × 1.101 × 1.028 × 1.050 = 1.84 → +84%

The 28.6% feels much more real though, so I’m sticking with current methodology. And it’s still too early to attribute it to anything other than luck - fully expecting down months and longer down-stretches to happen.

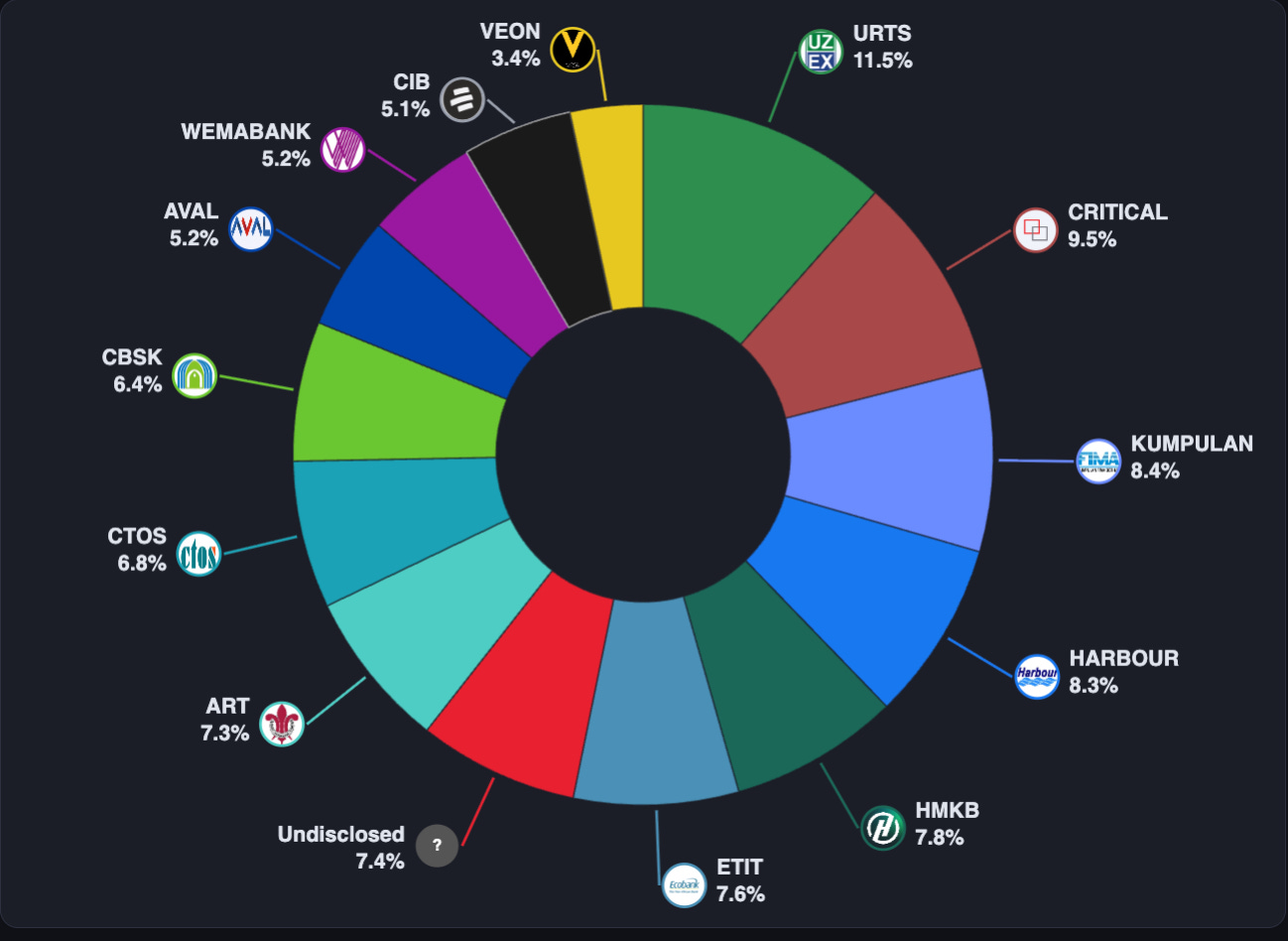

Pie chart:

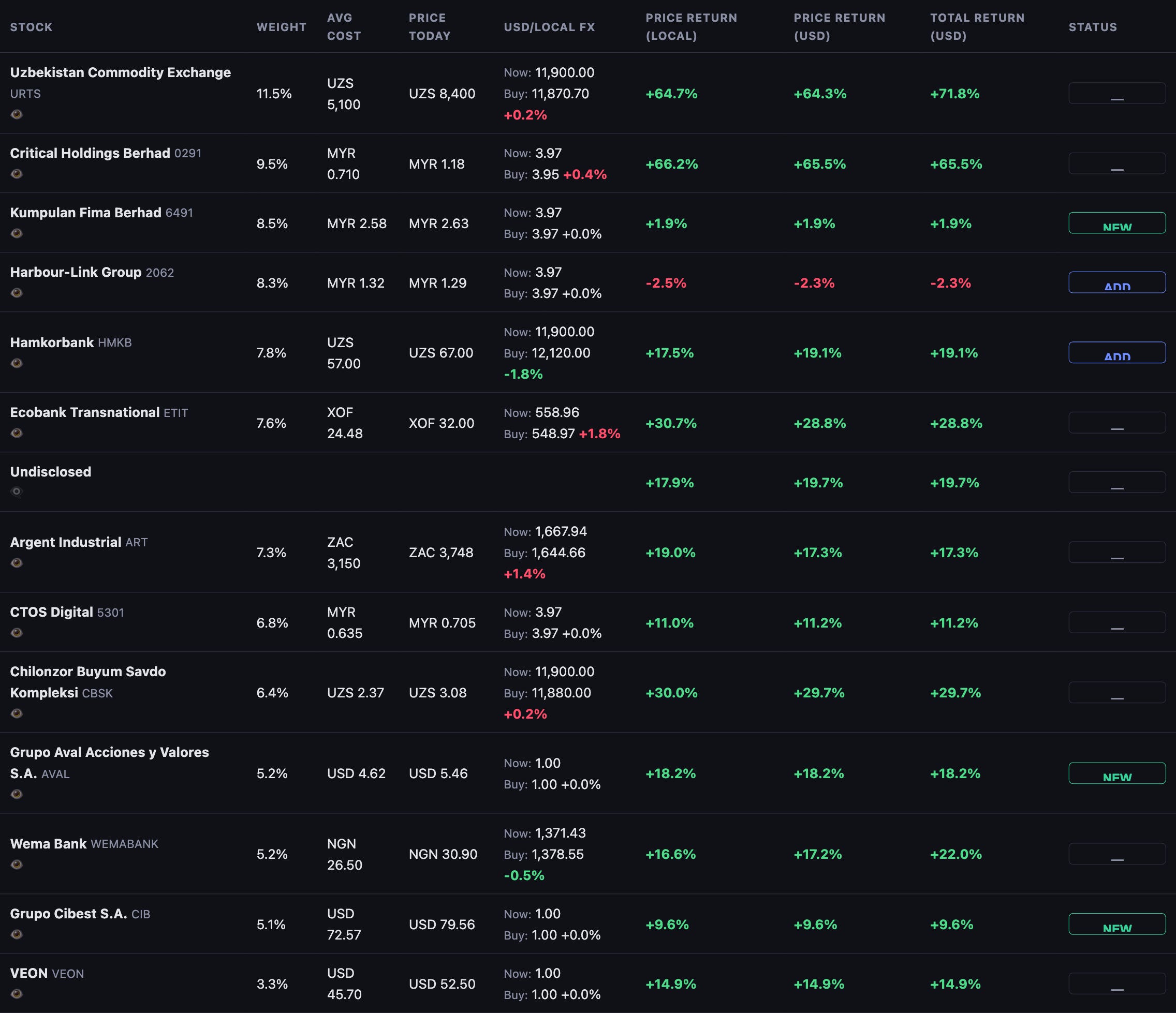

Full details:

Adds

Hamkorbank

Uzbekistan’s economy keeps doing really well. Mirziyoyev's reform trajectory keeps going: currency liberalization, privatization of state-owned banks (which helps a well-run private bank like Hamkorbank take share), a WTO-accession path, and record FDI into manufacturing/logistics/urban development. Real GDP growth is forecasted at a fantastic 6.8% for 2026 (Source: IMF). The latest inflation figures for May were 5.5% down from 7.0% in April. As inflation falls, rate cuts should follow, lifting the justified multiple on every Uzbek asset.

And Hamkorbank at 57 UZS was at the same price as when I originally bought it, and still a really cheap (P/E 4.5) well run bank with low non-performing loans, ROE 30% - growing at 20%-30%. So I bought some more.

Harbour-Link

Harbour-Link reported quarterly results on 28 May 2026: -29% net profit, and even worse -46% profit attributable to owners. Very ugly headline numbers and the stock was down 6.4% to 1.30.

But the weakness was driven mainly by scheduled vessel dry-docking/maintenance and engine overhaul, not a demand collapse. Management expects utilization and cargo volumes to normalize as vessels return to service. Integrated Logistics (the freight-rate-independent part) actually grew 9M PBT +23% with expanding margins. The balance sheet got stronger, with ~404M MYR net cash/securities versus ~500-520M MYR market cap. On normalized cash generation, the operating business is being valued at roughly ~1-1.5x EV/FCF.

Thought the drop was a great buying opportunity, not a thesis break.

New Positions

Kumpulan Fima Berhad

Covered here:

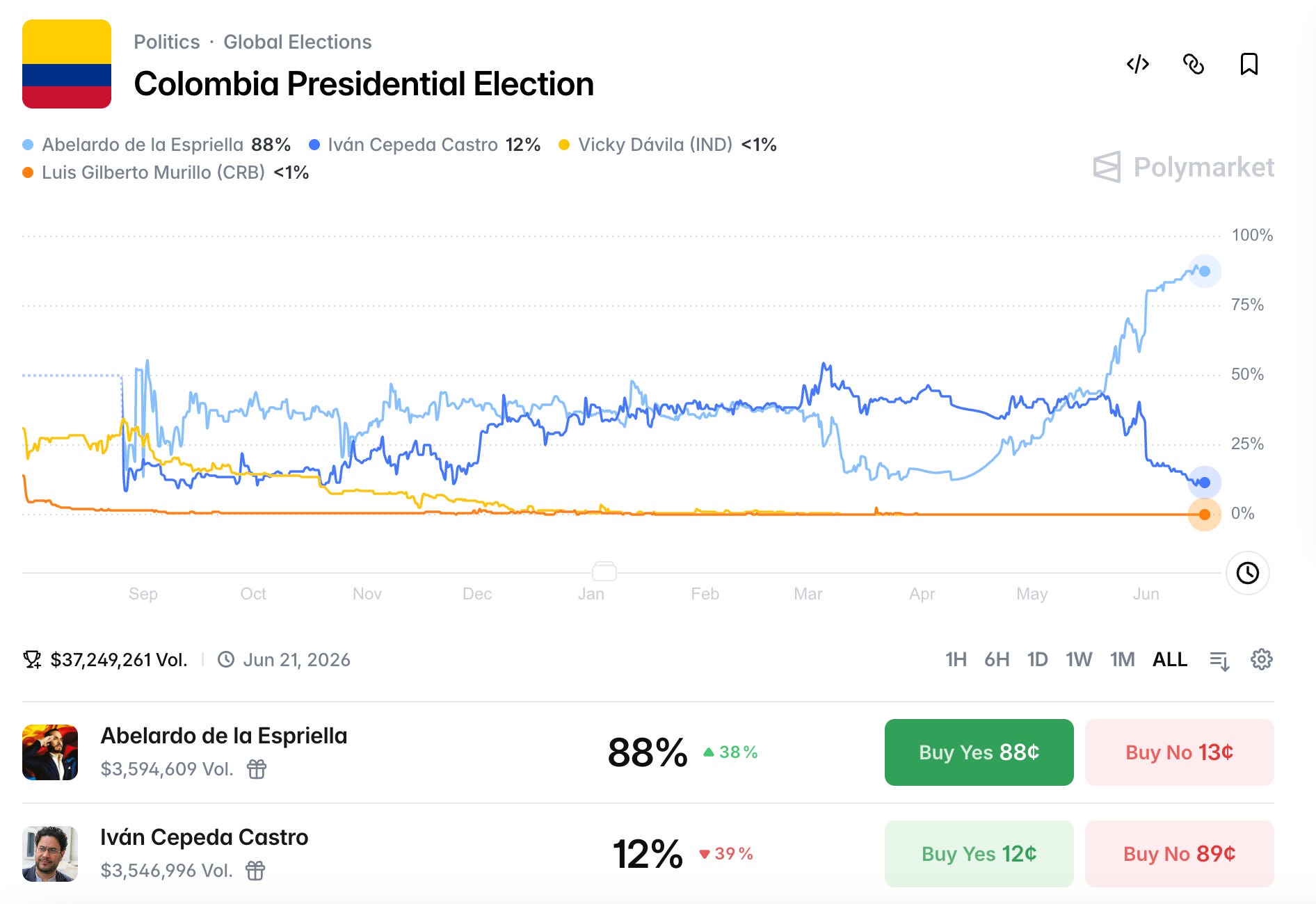

The Colombian Banks

Since I sold Millicom I have been looking for something to replace it with in Latin America. Saw this opportunity with the elections in Colombia. Equities and especially banks had been depressed in Colombia due to political mismanagement and additional bank taxes imposed by the ruling left-wing government. Ahead of the first round I saw that polls had the left-wing candidate (Cepeda) winning, but Polymarket showed a surge for the right-wing opposition (led by de la Espriella). Prediction markets typically beat polls, and I thought equities were still priced for continued status quo, but an opposition win would be a huge upside. So it was a Pabrai-style heads I win, tails I don’t lose much situation, where I thought the probability for heads was underestimated.

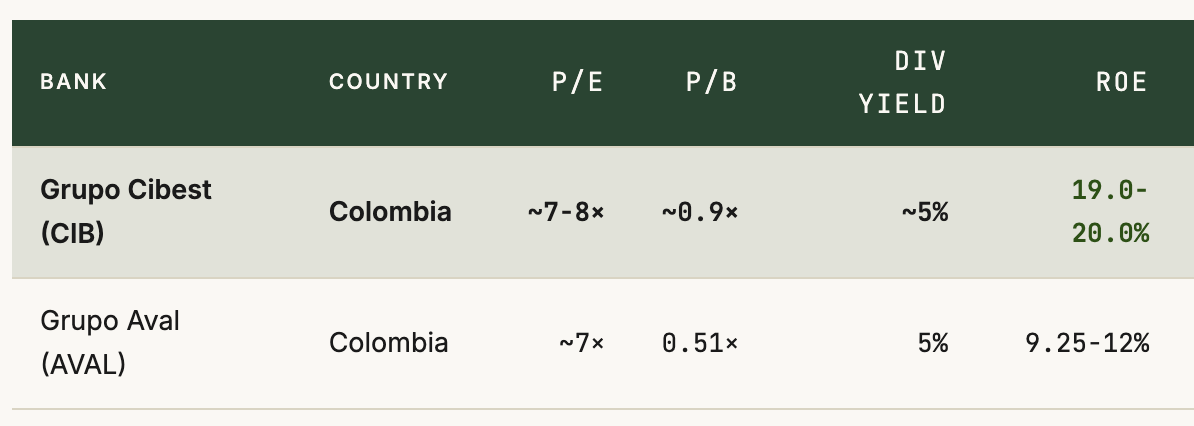

I normally have a preference for undiscovered small and microcaps, but there wasn’t time to open a local Colombian broker account, so I went with the two large high-quality Colombian banks listed in the US: Grupo Aval (AVAL) and Grupo Cibest (CIB).

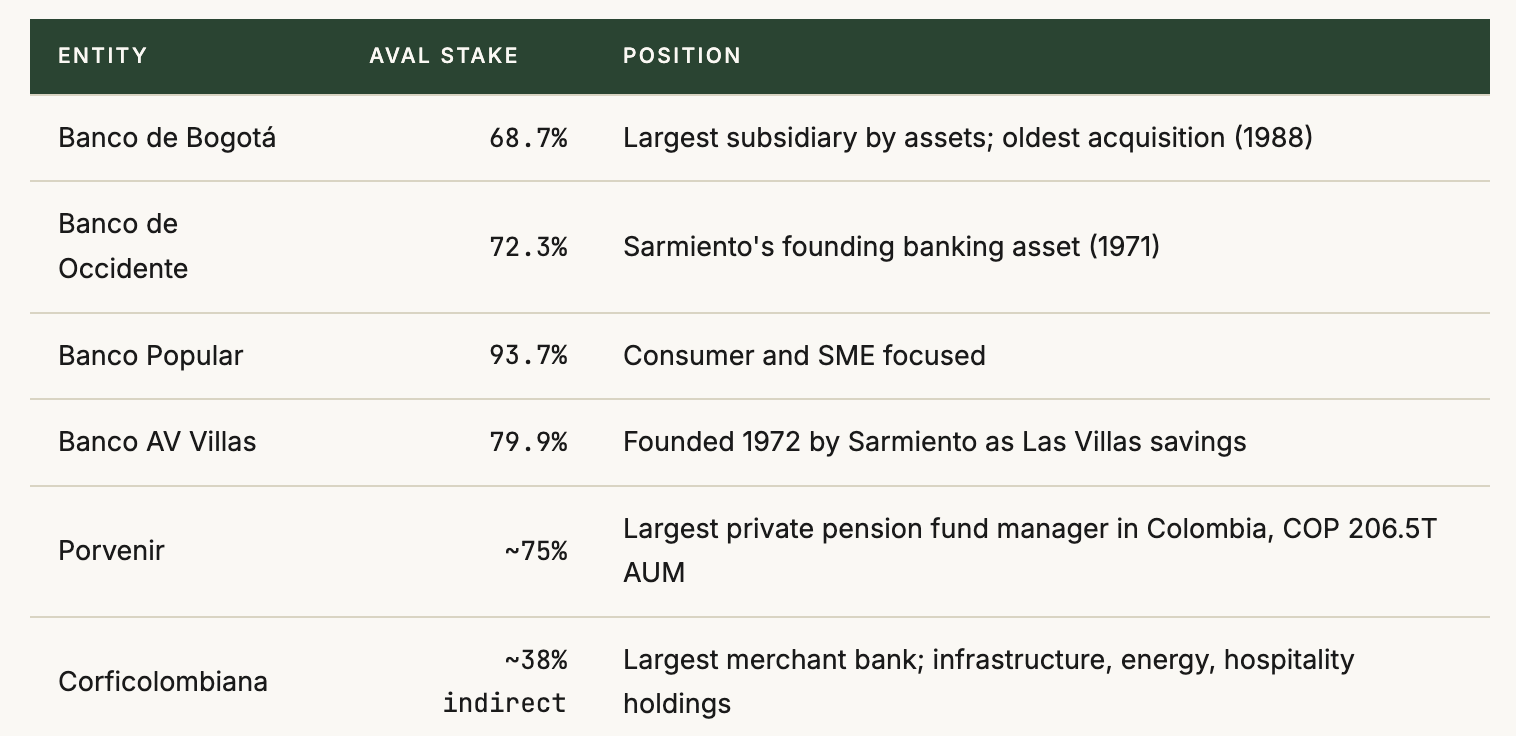

AVAL is a family controlled holding company for multiple Colombian banks:

AVAL had P/B of 0.51 at the time of purchase which is partly due to the holding company structure, but still remarkably low and lower than even Nigerian or Uzbek banks, giving a margin of safety. If one strips out a one-off tax for 2026, the underlying operational metrics for AVAL are fine: net interest income up 14.3%, NIM expansion of 39 basis points to 3.34%, deposit growth of 11.7% year-on-year, and a cost rationalization program targeting 9% savings on COP 1.4 trillion of controllable spend.

P/E at the time of purchase was 7, dividend yield 5% and ROE around 12%.

Grupo Cibest (CIB) owns Bancolombia which is Colombia’s largest commercial bank by assets, dominant in retail and corporate. It has two regional subsidiaries (Banco Agrícola in El Salvador, Banco Agromercantil in Guatemala), and increasingly material digital platforms (Nequi at 25.5 million accounts, Wompi merchant payments at breakeven with 55,000+ active merchants).

CIB has meaningfully higher quality than AVAL and other Colombian financial institutions in general - Q1 2026 reported ROE of 15% consolidated and 19% for standalone Bancolombia, with FY2026 guidance raised to 19.5-20% ROE alongside NIM guidance raised to 7.0-7.2%. It is also accelerating capital returns with a COP 4.3 trillion ordinary dividend declared (14.6% YoY increase, 60% payout ratio), plus a new COP 1.35 trillion share buyback program over three years signaling management confidence in capital generation.

CIB traded at P/E 7.5 when I started looking at it and had a P/B of 0.9.

But then I thought AVAL would have the biggest impact from the elections and bought it first, and waited a week to buy CIB, missing out on 10%. The market is catching on that there is a likely political change coming, so the re-rating has started, but I think there is still a pretty big remaining upside. And if meaningful reforms start after the elections, I’d like to be invested in Colombian equities long term, but as mentioned, I’m afraid that Latin American countries have a tendency to disappoint.

88% - 12% at the moment: