A Weird Conglomerate

Pineapples, passports, plantations, ports - somehow it works

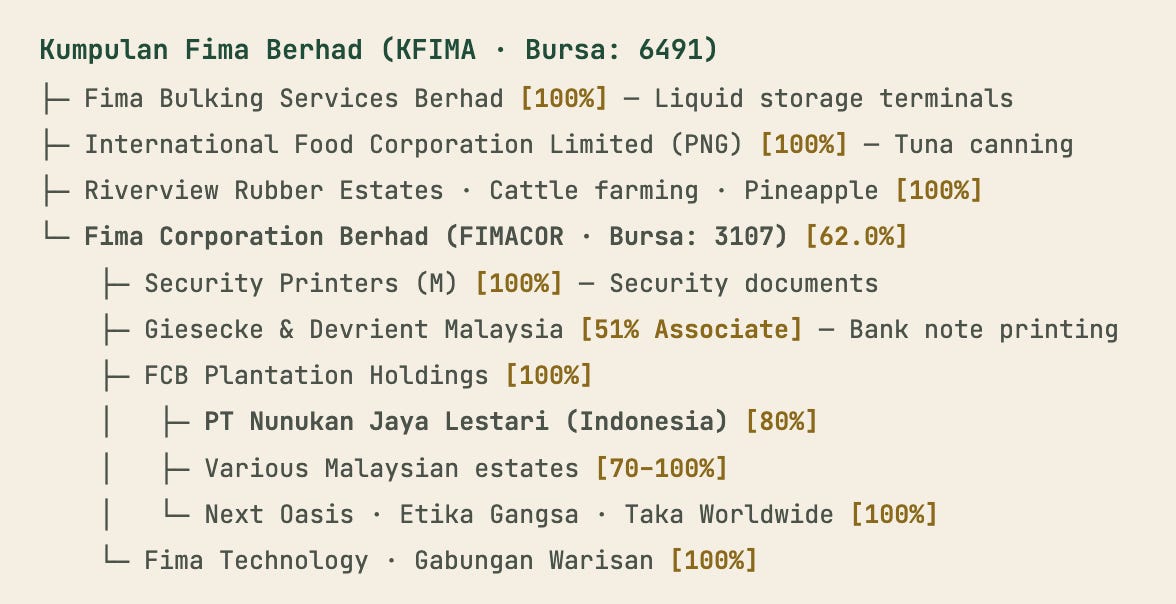

I found (yet) another interesting company in Malaysia! It’s KFIMA - Kumpulan Fima - a conglomerate with a very disparate set of activities:

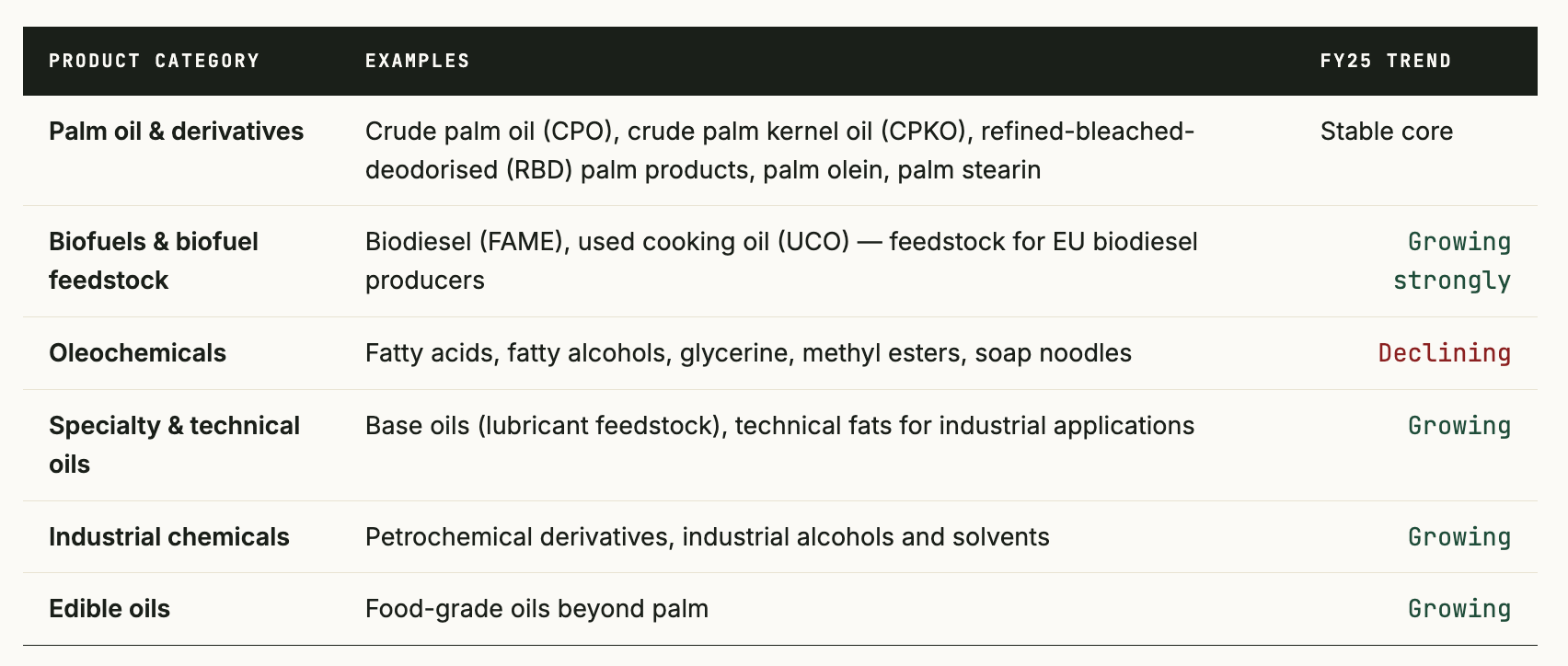

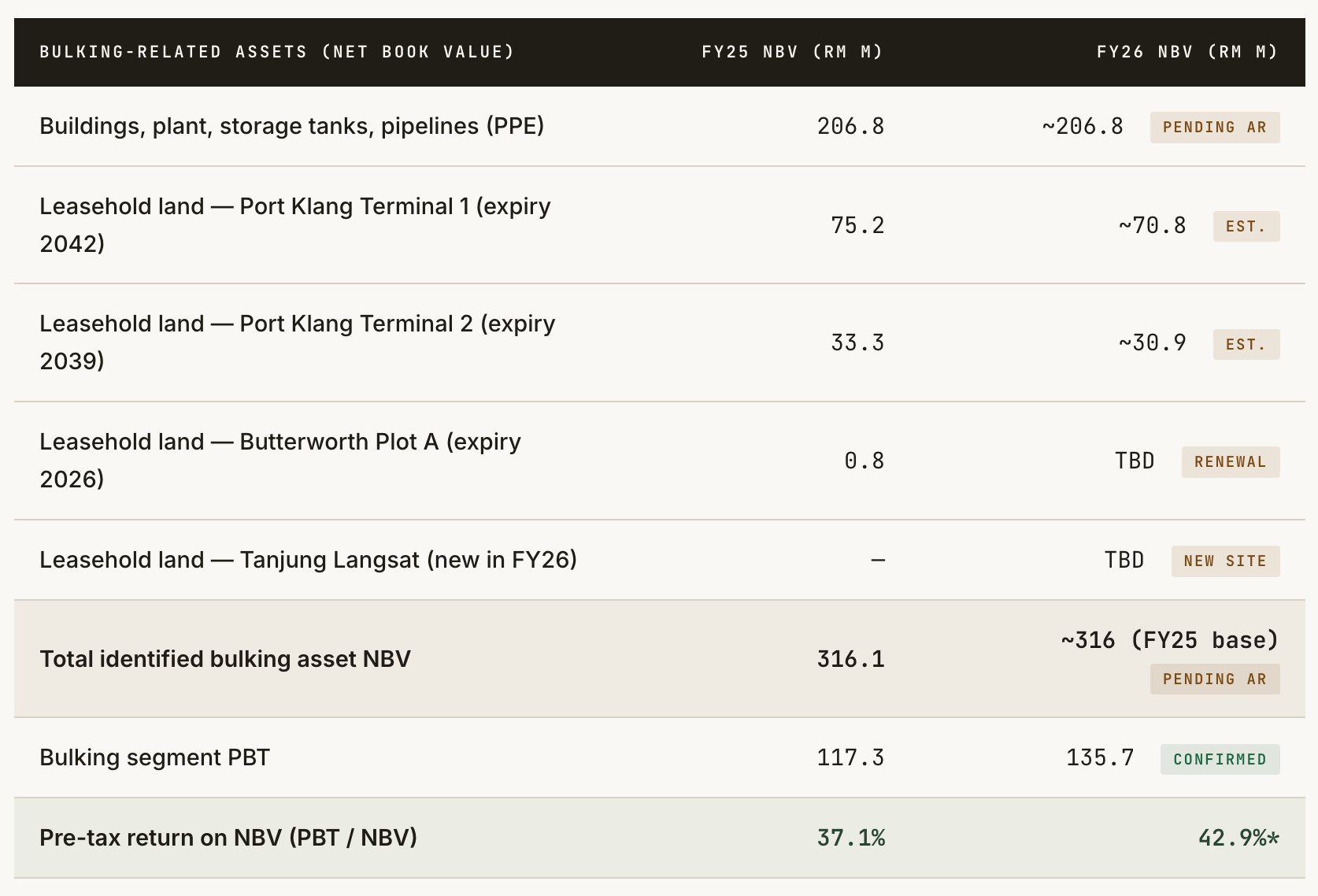

The biggest activity is so called “bulking”, which in KFIMA’s case means owning storage tanks for palm oil, biofuels, industrial chemicals, edible oils. These tanks are on land leased from port authorities in Malaysia on long leaseholds (expiring from 2039 to 2082, plus a small plot expiring this year) that normally get renewed.

Clients pay rent on tankage capacity, throughput fees on volume handled, and fees for value-added services such as heating (palm oil and similar products solidify at ambient temperatures and require handling temperatures of 35-50°C), filtration, nitrogen blanketing (the process of filling a liquid storage tank with inert nitrogen gas displacing oxygen and moisture, effectively preventing fires, explosions, oxidation, and equipment corrosion), drumming (bulk-to-drum transfers for downstream distribution), customs declaration and freight forwarding, containerisation and transhipment, trucking and related logistics.

The fixed cost base is dominated by depreciation on the tanks themselves, with limited variable cost beyond utilities and skeleton operating staff. Once a tank terminal is built and commissioned, the marginal cost of accommodating an additional tonne of throughput is near zero.

It’s a nice high margin business functioning as a port-toll franchise. And it’s growing, especially thanks to biofuels. Malaysia is becoming a regional hub for biofuel and used cooking oil aggregation serving EU demand under the Renewable Energy Directive (RED II/III). Used Cooking Oil collected across Southeast Asia is processed and consolidated in Malaysia before shipment to EU biodiesel producers.

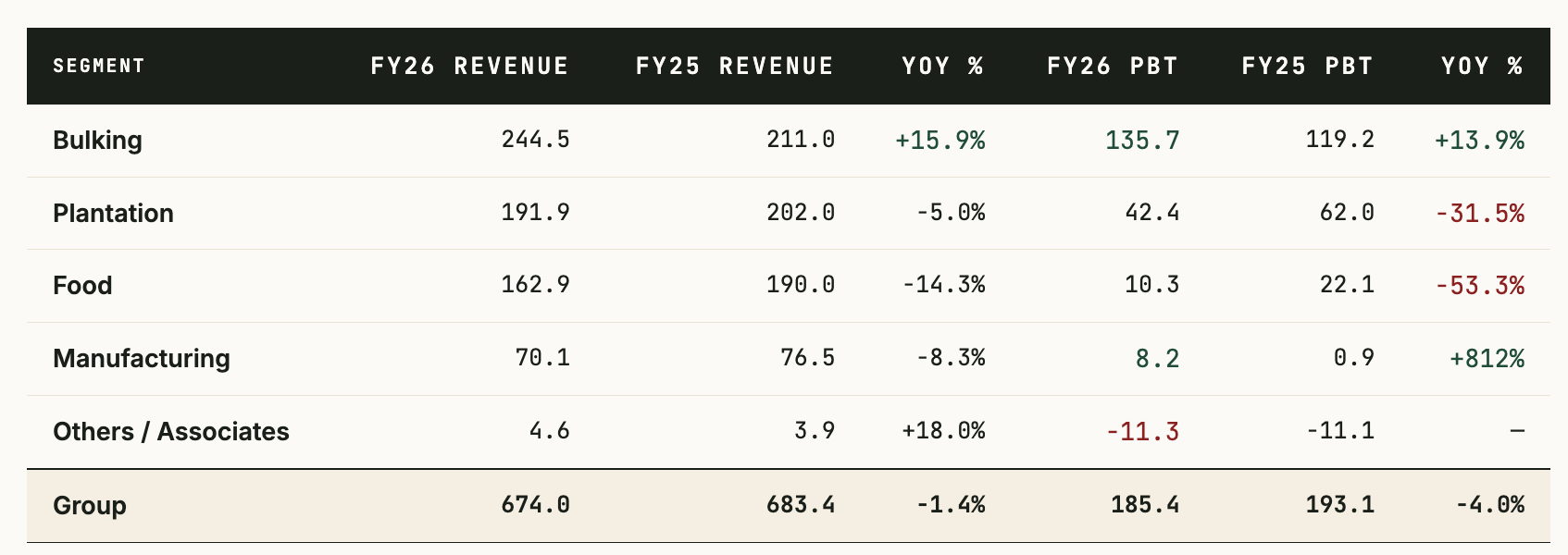

Looking at the book value of the tank terminals, they were at 316M MYR FY2025, and for FY2026 (1 April 2025 to 31 March 2026) they generated 135.7M MYR profit before tax giving a PBT/Book value ratio of around 40%. Pretty good for a physical business.

The thing is that in the FY2025 report (Note 14), it was disclosed that 261.1M MYR of property, plant and equipment is fully depreciated but still in operational use. The implication is that the operational asset base supporting current cash generation is materially larger than the reported PPE book value suggests, and that the annual depreciation charge of 33.2M MYR substantially overstates true maintenance capital expenditure requirements. A meaningful portion of current revenue is being generated on plant that costs nothing in accounting depreciation to maintain.

Papua New Guinea Fish(y) Business

Next up, we have wholly owned subsidiary International Food Corporation (PNG). PNG stands for Papua New Guinea - a proper frontier market!

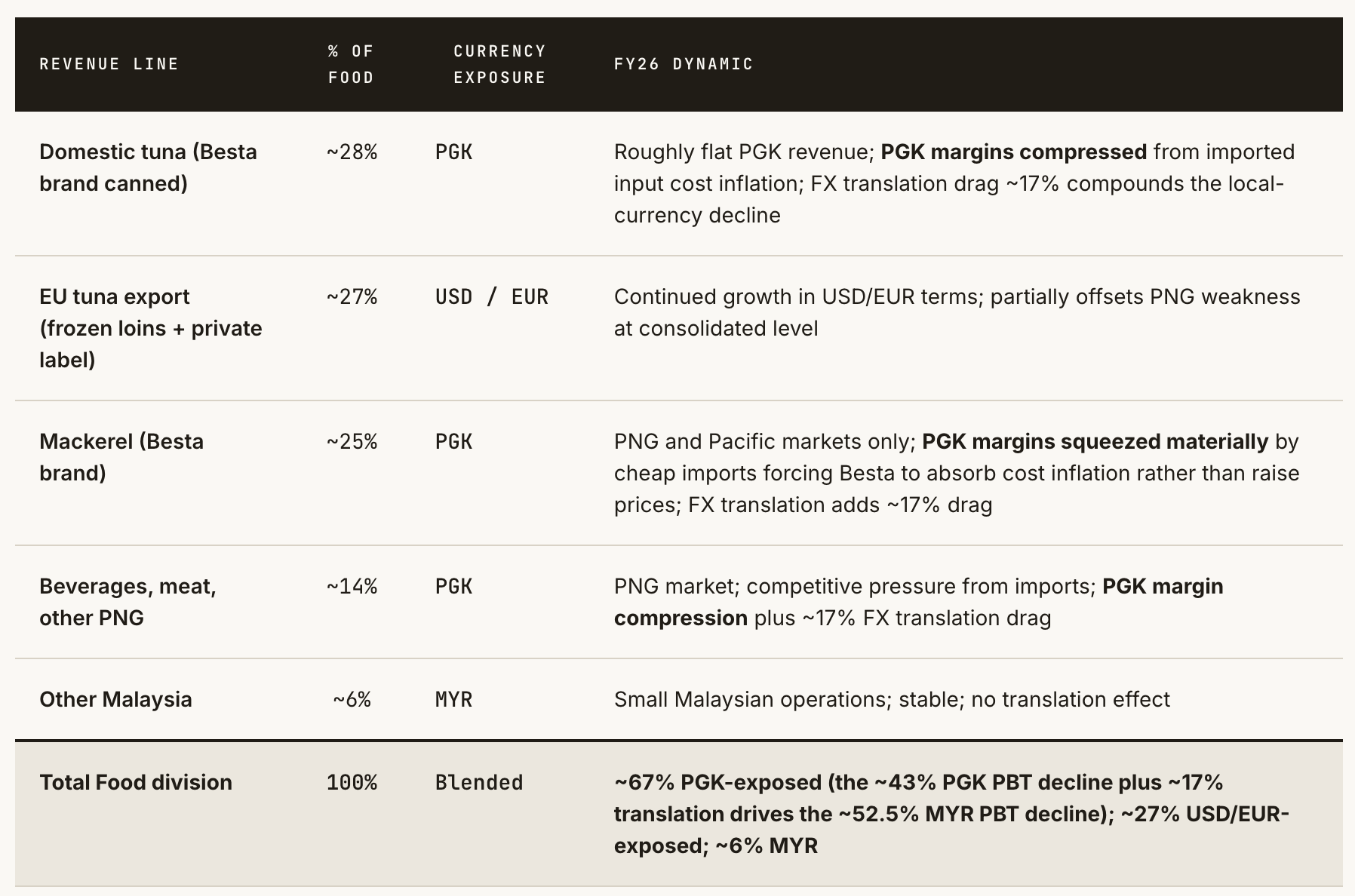

They produce canned Mackerel and Tuna and plenty of other foods and beverages under the Besta brand in Lae, Papua New Guinea. Apparently Besta is one very well recognised food brand on PNG. Most of it is for the local market, but they export some to the EU, as the EU has no custom duties on imports from PNG.

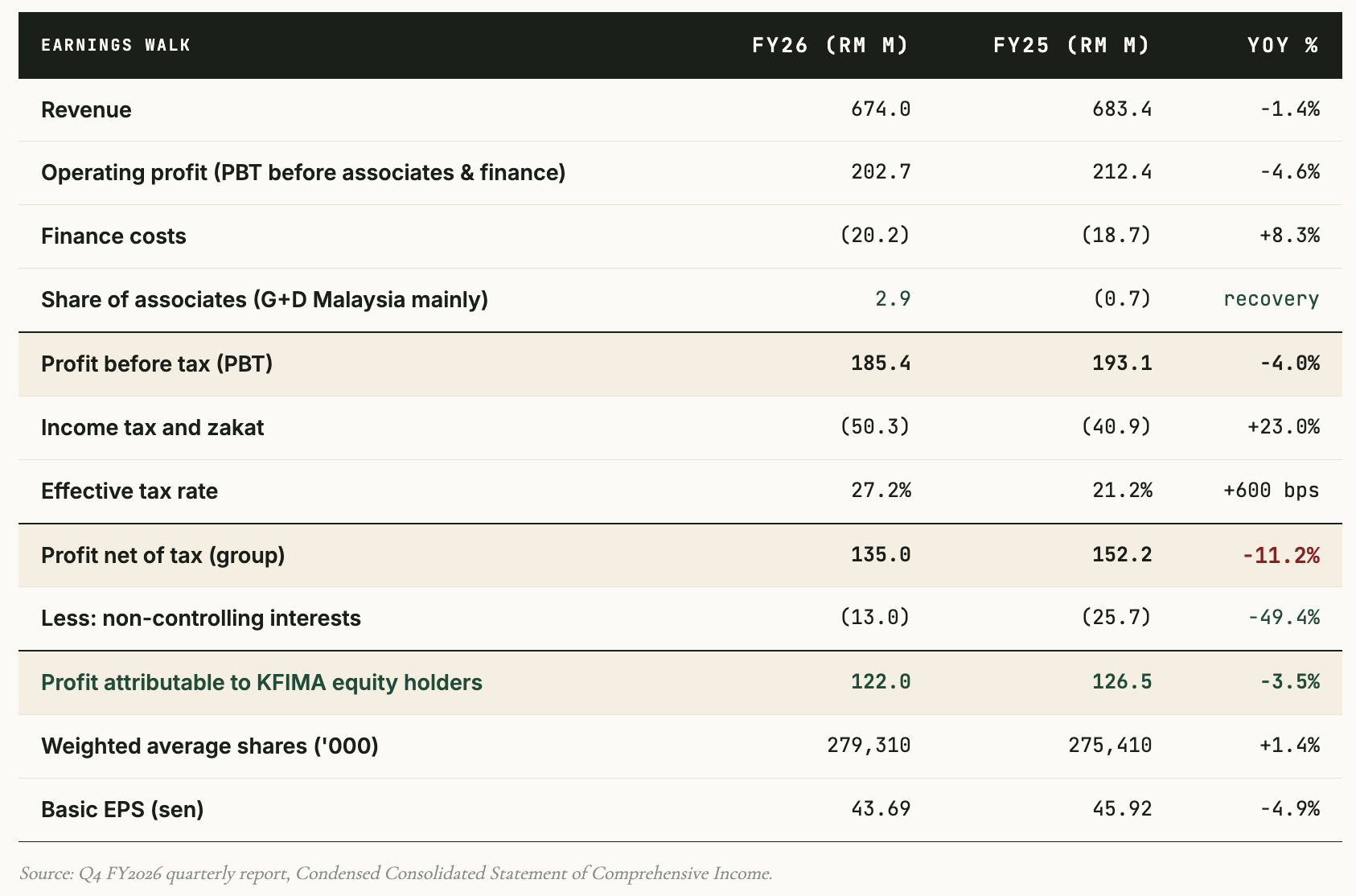

The results for FY2026 were reported 21 May 2026, and they were actually really bad for International Food Corporation, down 53.3% in MYR terms, from 21.9M Profit Before Tax FY2025 to 10.4M for FY2026. Revenues in the currency of Papua New Guinea - the Kina (PGK) - were flat, the problem was currency depreciation and margin compression. All their imported input costs went up, and local costs went up too with inflation, but they couldn’t raise prices because of competition from cheap imports.

PNG’s macro situation is a bit unusual in that it runs massive current account surpluses (17.4% of GDP in 2024, projected 22.5% in 2026) from natural resource exports, yet maintains chronic FX shortages, and conversions from PGK to USD are restricted. The explanation is that export proceeds are largely not repatriated to PNG - they remain offshore in USD accounts held by mining (gold, copper) /LNG/agricultural operators and other exporters.

From the exporters perspective, why bring in more than what’s absolutely needed into a currency that depreciates, where conversions back to USD are restricted, under a government that has a history of contract renegotiation, and retroactive tax changes.

So it’s a bit self reinforcing, the less funds are repatriated, the worse it gets (PGK depreciates, government USD debt service costs more), and the worse it gets, the less companies want to repatriate funds.

So it’s a somewhat tricky situation, could be made better by showing credible fiscal discipline, or by some planned mega-projects in LNG and gold getting going that would increase local investments/spend and bring in more tax and royalty payment to the PNG Government.

Now, the International Food Corporation is no longer such a big part of KFIMA, so even if it stays at current depressed levels or deteriorates further, it does not impact the KFIMA level results very much. And there is optionality in if things improve, and in International Food Corporation’s Export and Malaysian businesses growing.

KFIMA ex-FIMACOR

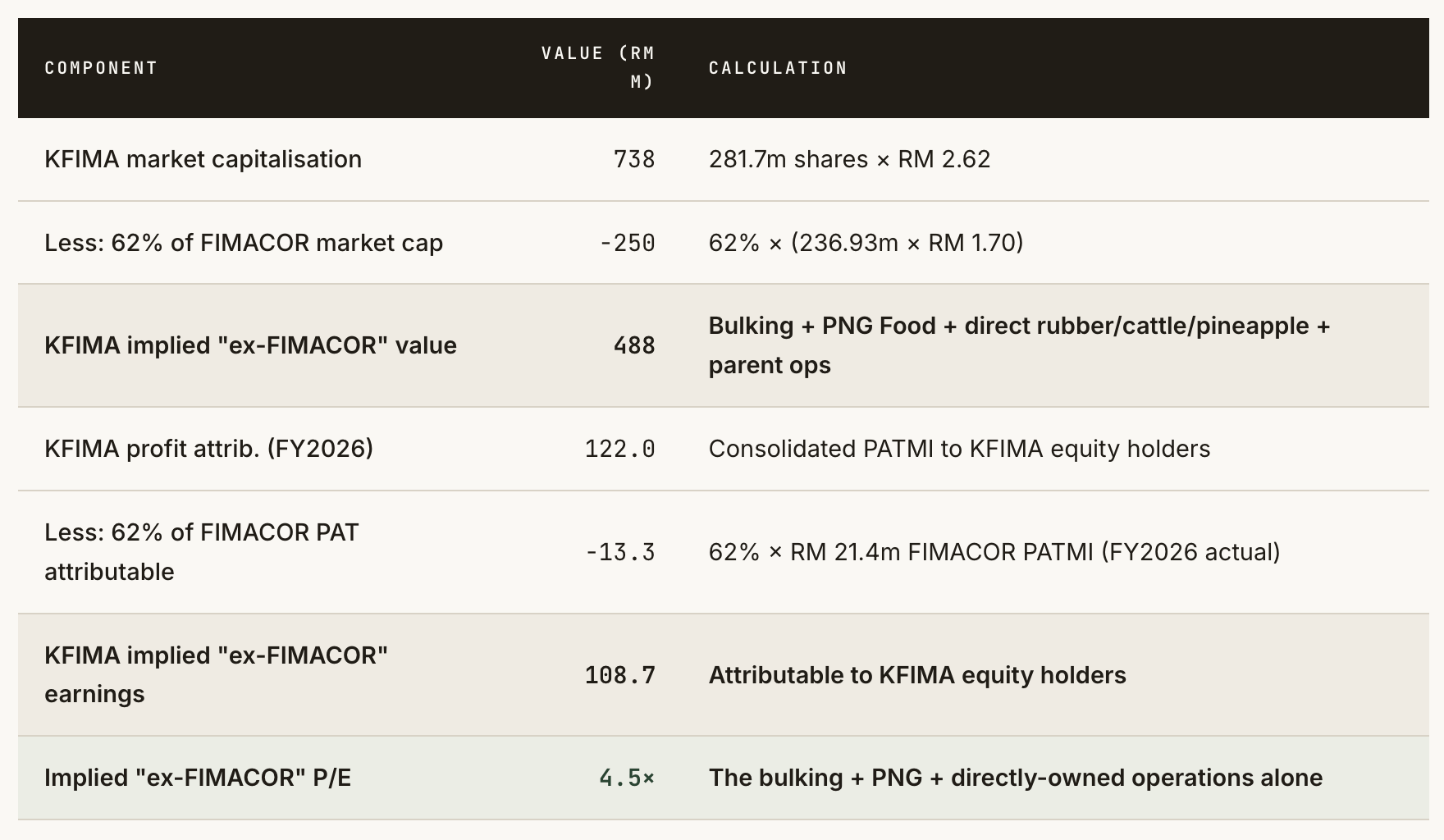

So if we stop here and look at KFIMA without the 62% owned listed subsidiary FIMACOR, we have the Bulking, the Food business in PNG and some rubber/cattle/pineapple businesses that aren’t broken out so I assume they are quite small.

The available breakdown is:

So if we take the 122M MYR Profit After Tax for KFIMA equity holders for FY2026, subtract the FIMACOR FY2026 Profit After Tax, we get 108,7M MYR , implying a KFIMA without FIMACOR P/E of 4.5, at KFIMA (2.62) and FIMACOR (1.70) stock prices as at Friday 22 May 2026.

FIMACOR

So what is FIMACOR? It is a Malaysian listed company that owns palm oil plantations in Indonesia (Borneo) and in Malaysia (Borneo and Peninsular Malaysia), plus a Security Document printing business and a 51% stake in Giesecke & Devrient Currency Technology Malaysia banknote printing business. Plus a small property management business.

The Indonesian plantations had a bad FY2026 (1 April 2025 to 31 March 2026), with lower sales, lower prices in Indonesian local currency, a depreciating Indonesian currency, and a 3M MYR one off loss due to wildlife incursion. They don’t say what animals it was - but this company has the most diverse set of risks I’ve seen!

One would expect the Indonesian plantations to recover for FY2027, but this is somewhat hampered by a new Indonesian regulation requiring all palm oil exports to pass through a government entity that presumably will take a cut of the profits, and make exporting more difficult and bureaucratic. Still unclear how things will work out, but this could push up palm oil prices, and be good for the bulking business and the Malaysian plantations. Further, the Indonesian government is mulling to reclassify some of the Indonesian plantation land to forest.

As to the Malaysian plantations, they are still maturing, and have been loss making the last two years, but are expected to give better and better yields every year going forward. Years 7-20 are the peak years of palm trees used to produce palm oil, and when the Malaysia plantations reach this phase PBT could 30M to 45M MYR.

I don’t love the plantations business - it is a commodity business with no pricing power and subject to political whims. But I have to recognise that the asset value of the plantations even at low estimates are above the whole market value of FIMACOR (417M MYR).

And why is it so cheap? It’s not the Indonesian troubles, the stock price didn’t budge on those. It’s more likely to be conglomerate discount just for FIMACOR. So KFIMA is conglomerate discount on conglomerate discount!

Then for both KFIMA and FIMA you also have the absence of professional analyst coverage, the limited institutional ownership, the small-cap liquidity constraint, the family control structure, and the multi-segment complexity.

Then we have the printing business called “Manufacturing” in the breakdown table above. Of course a Palm oil plantation business needs to print passports and banknotes on the side!

They have “Security Printing” that prints the following:

Travel documents: Malaysian passports (formerly a major contract, current status uncertain), visas, immigration documents

Licenses: Driving licenses, vocational licenses, professional credentials

Confidential documents: Examination papers and test materials, lottery tickets, tax stamps, education certificates

Banking documents: Cheques, bank statements, secure account documents

Government secure documents: Various ministry forms requiring authentication

And then FIMACOR has a joint venture with German company Giesecke+Devrient (G+D) for an entity called Giesecke+Devrient Currency Technology Malaysia Sdn Bhd. FIMACOR owns 51% and G+D Germany owns the remaining 49%. Despite FIMACOR’s majority stake, the JV is reported as an equity-accounted associate rather than fully consolidated, so this shows up in the Others/Associates line in the breakdown above.

Giesecke+Devrient (G+D) is a German privately-held company founded in 1852, headquartered in Munich. It’s one of the world’s three dominant banknote printers, alongside De La Rue (UK) and Crane Currency (US). G+D is also a major player in payment cards, currency authentication, secure SIM cards, government identity solutions, and cybersecurity. The company is family-owned, with revenue around €3 billion globally.

The Security Printing part contributed only to 0.9M MYR PBT for FY2025, but they invested in refurbishing and buying advanced machinery, won a contract and PBT went up to 8.2M MYR FY2026. G+D Malaysia went from 2M MYR loss FY2025 to 2.9M profit FY2026.

Here are the full printing numbers plus estimates for FY2027

It’s an ok business, and FY2025 was burdened by one off refurbishment costs (of intaglio machines). I estimate it will keep making money, but not grow much above FY2027 estimates. And long term there is a digitalization trend that is a headwind, even if the stuff they are printing is likely the last to fall to digitalization. Will we have digital passports, digital driving licenses in the future? Yeah, probably. Will all cash disappear? Probably not.

The People Behind KFIMA

KFIMA was incorporated by the Malaysian Government in 1972 as Fima Sdn Bhd (”Food Industries of Malaysia”) starting with pineapple canning. In 1991, the company underwent a Management Buy-Out led by Tan Sri Basir Ismail (1927-2007) - a Taiping-born, Nottingham-educated agronomist who concurrently chaired the Malaysian Palm Oil Board, Malaysia Airports Holdings, and Bank Bumiputra, and was instrumental in bringing Formula 1 to Malaysia. Listed on Bursa Malaysia in 1996. Following Basir’s death from a heart attack in 2007, ownership passed to his four children (Ahmad Riza, Roshayati, Rozilawati, and Rozana Zeti Basir) who collectively control approximately 48% via the family’s private vehicle BHR Enterprise Sdn Bhd plus direct holdings - with Rozilawati (19%), Roshayati (~18%), and a third family entity (~17%) as the three largest shareholders. Day-to-day operations are run by professional management under Chairman Dato’ Idris Kechot and Group MD Dato’ Roslan Hamir, with family members serving as non-executive directors providing oversight.

The structure is unusually stable. Per KFIMA's annual report disclosures, Puan Sri Datin Hamidah holds preference shares in BHR Enterprise carrying veto rights over all BHR decisions - providing matriarchal oversight one layer up from the operating company. Multi-generational family control with this veto preference structure is a governance model that prioritises long-term stewardship over short-term value extraction. The consistent dividend payment record (KFIMA has paid dividends every year since listing in 1996) and the disciplined capital allocation toward bulking expansion are consistent with this characterisation. The principal governance risk is intergenerational transition, which is a multi-decade rather than near-term concern.

Balance Sheet

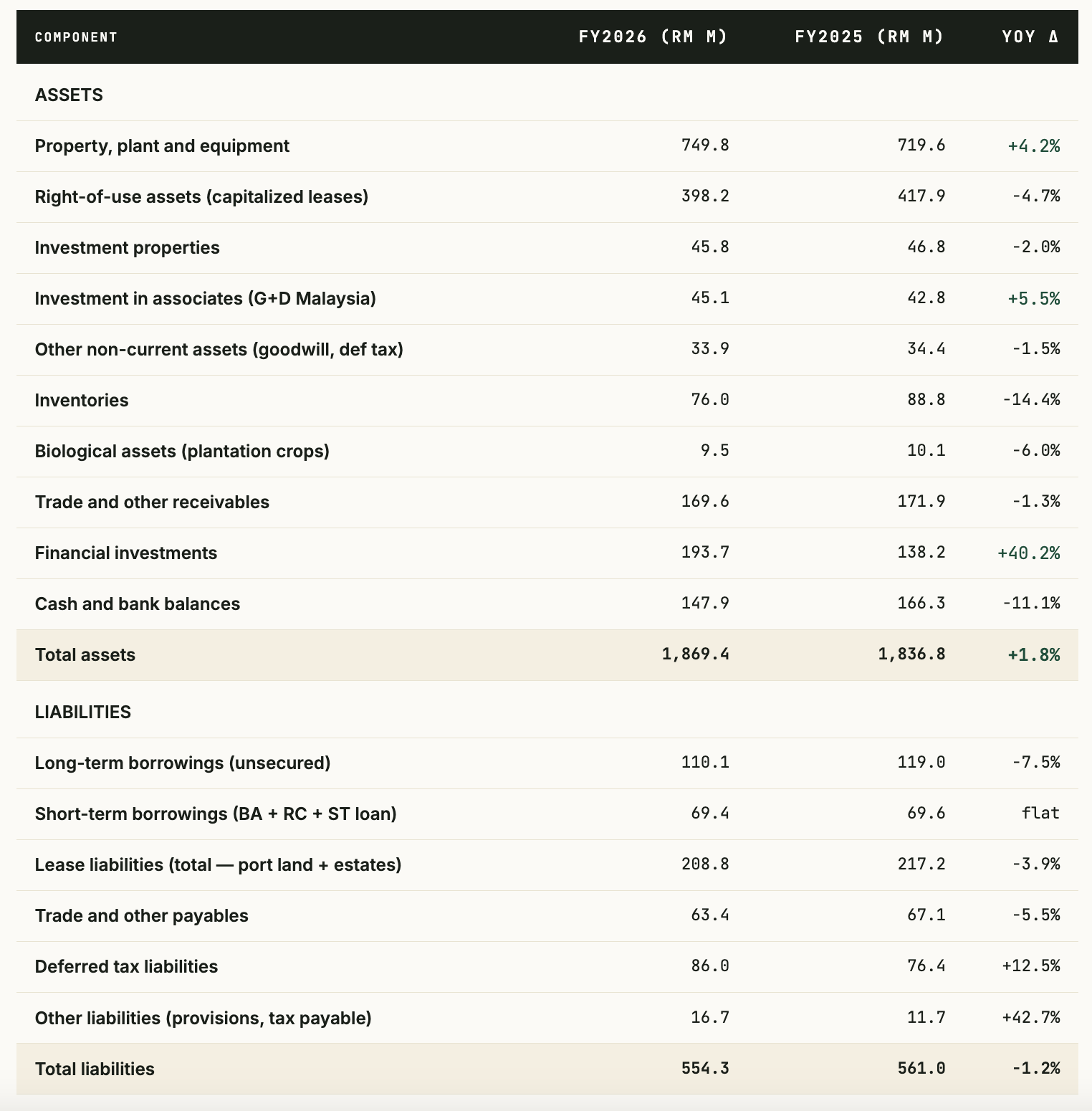

This is very strong, 162M MYR net cash, 0.68× book value, and the book values don't reflect the 261M MYR of fully-depreciated tank terminals still generating revenue (per Note 14 of the FY2025 annual report) or the plantation land carried at historical cost. The lease liabilities are matched against capitalised port land leases on the asset side.

Conclusion

When I first looked at this before the FY2026 results, they were investing in this new tank terminal, so free cashflow and other metrics didnt look as good, plus that the printing business wasn’t contributing. But one could see that there was a really good, very inexpensive business underneath. Now things are clearer, and the stock went up 5.2% on the report, despite the setbacks with Papua New Guinea and the Indonesian plantations.

I think the report confirmed the thesis and that KFIMA presents the unusual combination of a high-quality structural asset (the bulking franchise), trading at a valuation that more closely resembles a stressed cyclical than a port-infrastructure toll operator.

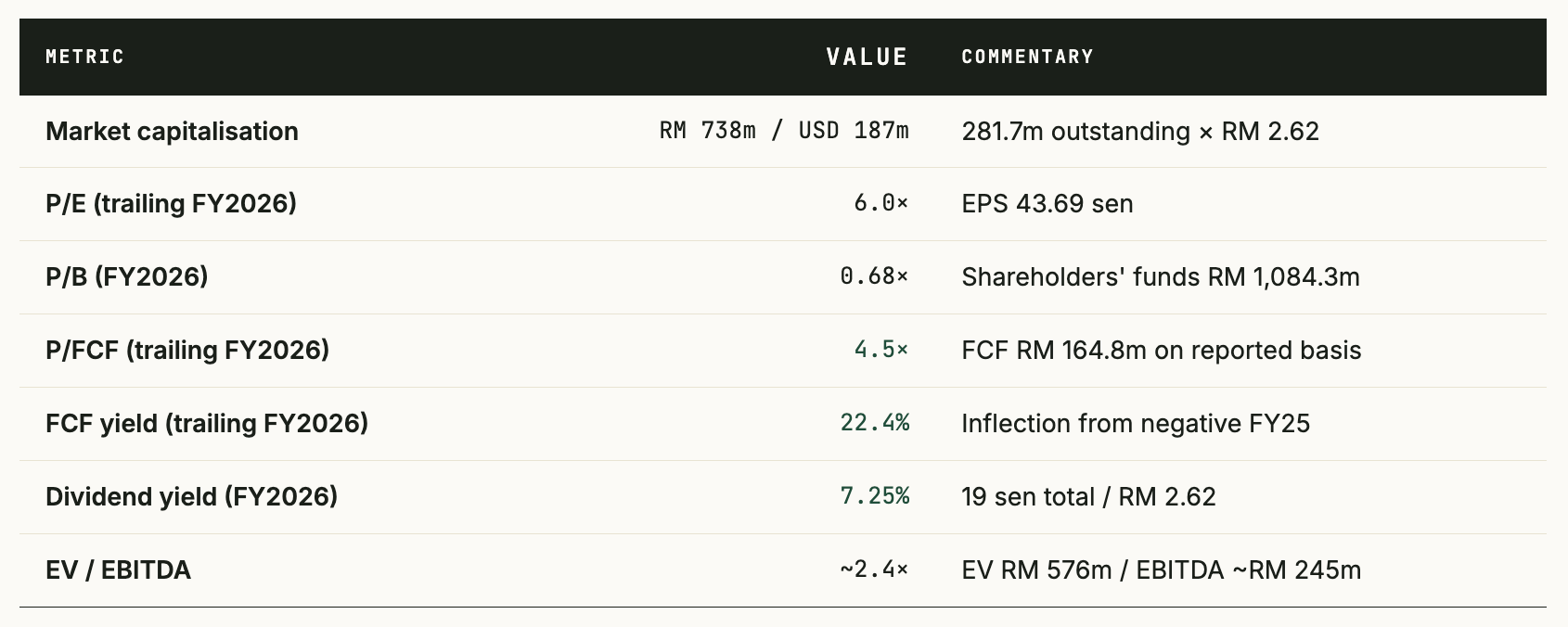

It’s still a small cap that is complicated to analyse, and the conglomerate discount will likely never go away, but there is still a lot of re-rating left. This table with consolidated metrics shows the situation:

And when the new terminal is up and running the normalized free cashflow will be even higher pushing P/FCF down to 3.7-4.1, even if the Malaysian plantations don’t mature and the Indonesian ones continue to misfire, and Papua New Guinea keeps messing up their currency.

The bulking franchise generates port-infrastructure cash flows but trades like a distressed plantation conglomerate. That gap is the investment opportunity. Until either the market recognises it, or operational results force the recognition. While waiting, it pays dividends of 7.25% that are well covered by operations.

KFIMA goes into the FrontierViking portfolio.