The Inconvenient Exchanges

Frontier and emerging-market bourses, screened for the ones the world is too lazy to buy

Noticing that CTOS Digital has reduced margins because of listing costs, and that Hong Lai Huat has multiple business lines that combined are not enough to pay the fee to be listed on the Singapore main board, I thought I should take a look at exchange owning stocks.

Exchanges are natural monopolies with network effects and multiple capital light income streams. They make money from:

Trading fees - small fees on each trade

Clearing/Settlement - fees from guaranteeing and settling trades, and from interest on pools of margin collateral

Listing fees - companies pay to list (IPO) and regularly to remain listed

Market Data - exchanges create market data, which is increasingly valuable

Indices - licensing benchmarks for ETFs/Funds, royalty model (typically negligible for frontier exchanges though)

Custody - recordkeeping of who owns what

Technology - co-location, feeds, trading access, for brokers/high-frequency trading

Once an exchange is up and running, and trusted and regulated, it attracts liquidity. Everybody wants to trade at the exchange with most liquidity, and more participants create more liquidity, so that’s a nice flywheel, that’s hard to break into by competitors.

So it’s a great high margin business model, especially when capital markets deepen, when markets formalize, and more savings go into pensions/funds, retail participation rises, capital markets take share from bank lending, and multiple markets develop/grow like derivatives markets.

There have been multiple studies showing that exchange owning stocks outperform the index of their own exchange.

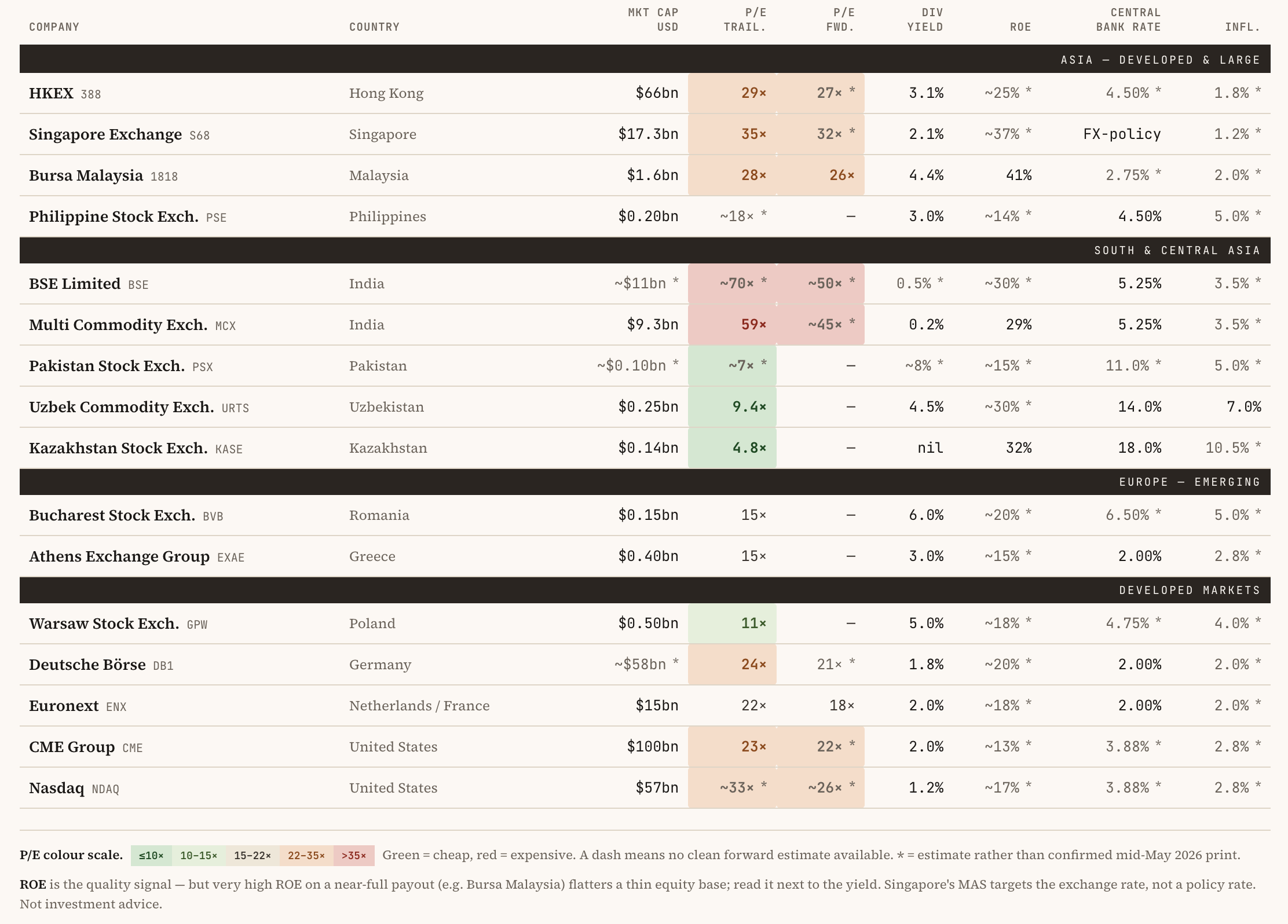

This hasn’t gone un-noticed of course, and exchange owning stocks typically trade at very high multiples. However, could there be inexpensive exchanges in Emerging/Frontier markets? I had Claude draw up a table and throw in some developed market exchanges as references:

Before the deep dives, here's where I land. Stripping out the too expensive ones or where the capital markets aren’t deepening, the shortlist that comes out of it is B3 (Brazil) and BYMA (Argentina) as FrontierViking portfolio candidates, URTS as this thesis already in the portfolio, and KASE, Dar es Salaam, Colombia and Pakistan as watchlist or access-friction names.

A few things that stand out from the table above:

The Nigerian exchange NGX at 37.5x trailing P/E. It had a run-up of 5x following Tinubu’s reforms. A clear pass now - yeah Im not paying 37.5x for Nigerian frontier market risk - but interesting if it ever gets cheap. At 12% of total stock market cap / GDP, it has a long runway.

The Indian exchanges are like the whole Indian market very expensive - I’m staying away.

The Johannesburg Stock Exchange looks cheap, but the problem is that capital markets in South Africa aren’t deepening, there is a multi-year delisting wave, and foreign outflows. Exchanges are resilient business models though, and the JSE will likely pay good yield and if things turnaround in South Africa, it could be great, I’ll need to see more signs of improving capital markets first though.

And we have URTS, the Uzbekistan Commodity Exchange that is already the largest holding in the FrontierViking portfolio. It has had a run-up, but is still inexpensive with a long runway ahead.

Bursa Malaysia has after a stagnant decade seen average trade volume go up, foreign flows coming back, and it has a strong IPO pipeline. The market has noticed though, and re-rating has happened. Too expensive, otherwise great.

Warsaw actually looks interesting, wonder why it is so cheap - but out of scope for the FrontierViking portfolio.

Others that look interesting from this initial analysis are BYMA (Argentina), B3 (Brazil), KASE (Kazakhstan), Latinex (Panama), and the Pakistan, Colombia, Mexico and Tanzania exchanges.

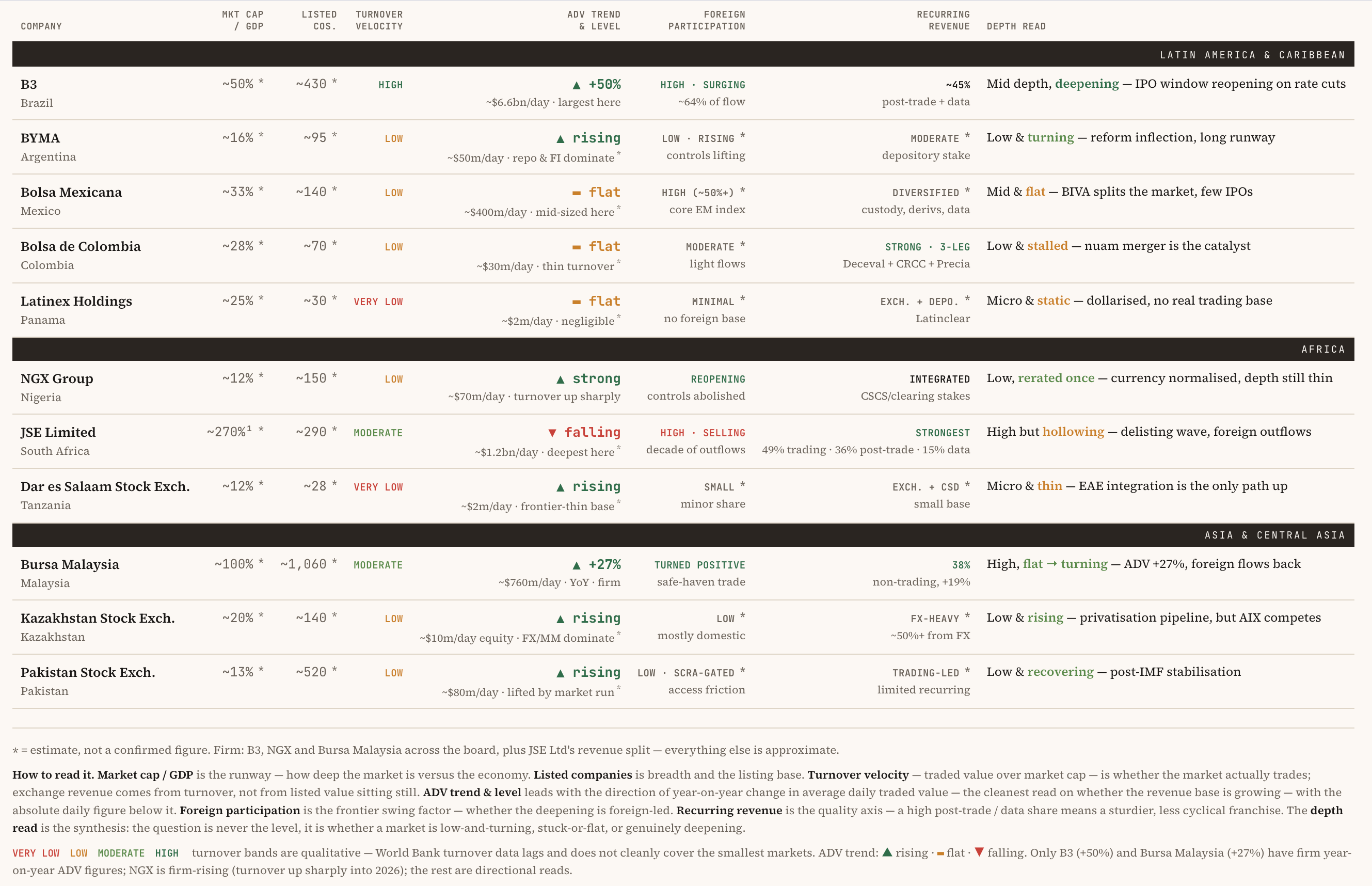

More data on the interesting ones, plus South Africa, Malaysia and Nigeria:

B3

For B3 in Brazil things are good and accelerating in the right direction, Average Daily Volume is up 50% year-on-year, Q1 revenue was at record levels, foreign inflows in Jan–Feb alone beat all of 2025. Turnover velocity is high. And B3 does clearing, settlement and depository in-house has ~45% recurring revenue, ~25% ROE, 70%+ margins.

It’s not super cheap though, especially given Brazil’s high interest rates and general macro situation that is not nearly as good as Malaysia or even Uzbekistan. However, the Brazil central bank rate - the Selic - has been cut twice recently, and if this trend continues it’s another tailwind for B3.

Then we have that it is an election year in Brazil. If Lula wins, it’s no change, that’s fine for B3. If Bolsonaro Jr wins, well he is the non-left wing candidate and has been campaiging on privatisations, spending cuts, tax-reform rollback, digitalization of the state to attract foreign investment. In theory better for B3, but then again one never knows with politics. I’m thinking that any non-left-wing candidate in Latin America, at least has to take a look at the success Javier Milei is having in Argentina.

BYMA

And speaking of Argentina, BYMA is the exchange with the most explosive upside. Argentina’s market is shallow, under-owned, and under-institutionalized, which creates a huge runway if disinflation and reform continue. BYMA is cheap enough that one is not paying perfection prices. It shouldn’t be valued 1/10th of Brazil’s leading exchange, and well, Argentina should be a much richer country than it is.

I recognise that Argentina has been the wrong country to invest in the last 100 years or so. Milei’s reforms to increase economic freedom across the board are a total break with the past though, and they are popular, and things are improving visibly. Still debt is high, reserves low, so the situation isn’t totally under control yet, but I don’t know any emerging/frontier market that is reforming in such a dedicated way.

I think the risk/reward for BYMA is great. It is a strong candidate to take Millicom’s spot in the FrontierViking portfolio (as is B3), but Argentina market access is a bit tricky. Argentina has many stocks listed in the US, but BYMA isn’t one of them. One has to open a local brokerage and get a tax document which can take a few weeks. Overcoming inconvenience is an edge after all, so I’ve started the process!

Kazakhstan Stock Exchange (KASE)

It’s really cheap, even adjusted for Kazakhstan’s high rates and inflation. Trends are in the right direction, but there are a few problems:

1) Kazakhstan deliberately runs two exchange ecosystems - KASE and the Astana International Exchange (AIX). AIX was built specifically to attract international listings and prestige mandates. So the privatisation pipeline that's supposed to be KASE's catalyst may not actually accrue to KASE.

2) It doesn’t pay dividends - not sure why, but not a great sign.

3) The National Bank of Kazakhstan holds roughly half the exchange - so it's a state-influenced entity.

4) About half of KASE's revenue is tied to FX and money-market activity, not equities. So even if the equity market deepens beautifully, it only touches part of the franchise - and the FX-heavy half is more exposed to currency regime and rate decisions than to capital-market development.

None of these is an individual dealbreaker - but the combination makes me wait and see with KASE.

Dar es Salaam Stock Exchange

One of the smallest and most undiscovered in the bunch. An exchange that is a nanocap. Revenue doubled since last year. Great runway. 12% market cap/GDP, and a fast growing population. It may have a catalyst in that the state gold-mining company has been in listing discussions - and for a venue this small, a single large resource listing is materially needle-moving: it adds listed-company count, market cap, trading volume, and listing fees all at once.

Tanzania has long been African Lions Fund’s largest individual country btw, and this fund has been the best performing Africa-fund I believe. Not sure if they hold the Dar es Salaam Stock Exchange though.

In conclusion this is very interesting. The one problem is access though. I’ve been trying to get access to the Tanzania stock exchange in the past - emailed two local brokerages, but none responded.

Bolsa de Valores de Colombia (BVC)

BVC owns the full exchange vertical, trading, post-trade, and data: Deceval (the central securities depository - custody), CRCC (the central counterparty clearing house), and Precia (the pricing and valuation vendor).

It’s a high quality exchange, the problem is that it has been flatlining.

It’s got two significant events coming up:

BVC is merging with the Santiago and Lima exchanges to form nuam, an integrated Andean exchange. Execution risk, but could get growth starting again.

Elections in Colombia, first round 31 May, second round in June. Potentially positive impact if Colombia follows the latam trend towards more market friendly leaders.

I’ll put this in wait and see.

Pakistan Stock Exchange (PSX)

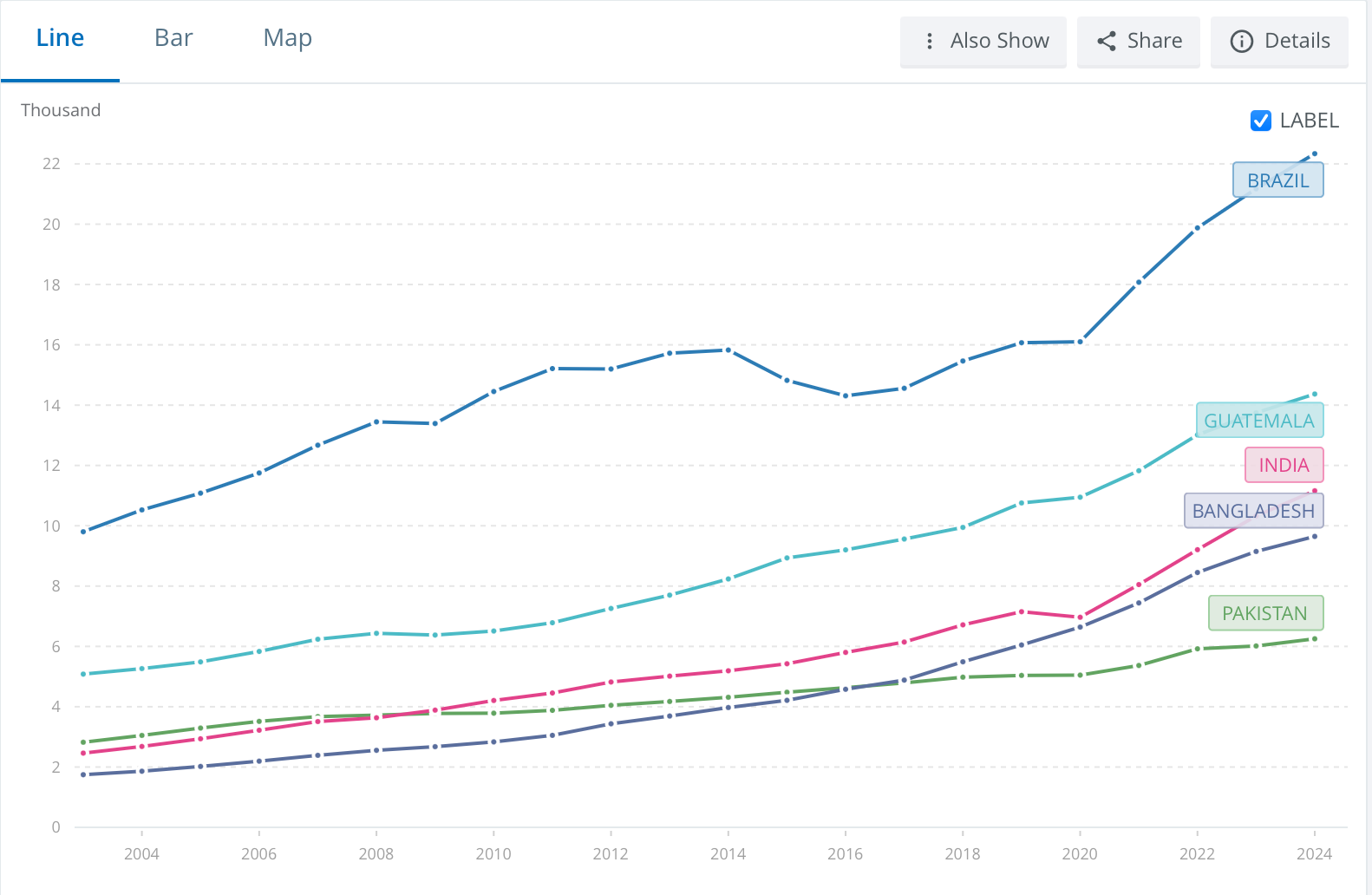

For being in a relatively poor country the PSX has real breadth: 520 listed companies, a functioning broker network, an established index. Long runway as Pakistan’s formal equity market is small relative to a ~250-million-person economy.

Pakistan’s macro is quite weak though, it has a long history of devaluing the currency and going on and off IMF programmes (even if the current one is possibly more promising). And Pakistan is stagnant in terms of growth, underperforming not only southeast Asia, or Latam, but also Bangladesh and India:

Then again, Pakistan has a thriving informal sector, not reflected in GDP numbers, and it has been very possible making money investing in listed Pakistan stocks despite the macro situation.

As to the PSX, it is trading-led, with limited recurring revenue. Its revenue rises and falls with trading activity, with little sticky post-trade or data income to cushion a downturn.

[Edit: A reader pointed out that PSX owns roughly half of NCCPL (National Clearing Company of Pakistan, and 40% of CDC (Central Depository Compnay) so it is less trading dominated than I thought.]

Getting access to Pakistan appears to be quite a hassle. At the moment I consider it not worth it. Got to find more interesting cases there first.

Finally Mexico and Panama seem stagnant.

Would add NUAM to the list

Nice overview! These are moaty and interesting businesses, often with very long history. There is also a certain irony in your qoute "There have been multiple studies showing that exchange owning stocks outperform the index of their own exchange."

One factor worth considering is ownership structure. I have looked at the Philippine Stock Exchange, though it seemed a bit too expensive, and also the Budapest Stock Exchange. In the latter case, I am not comfortable with the very high level of state ownership. It raises questions around incentives, commercial drive, capital allocation, and alignment with minority shareholders.

Is ownership structure something you factor into your analysis of exchange operators? Or rather, how much?