Floebertus Style Bubble Chart and Big Tycoon Risk

More Malaysia

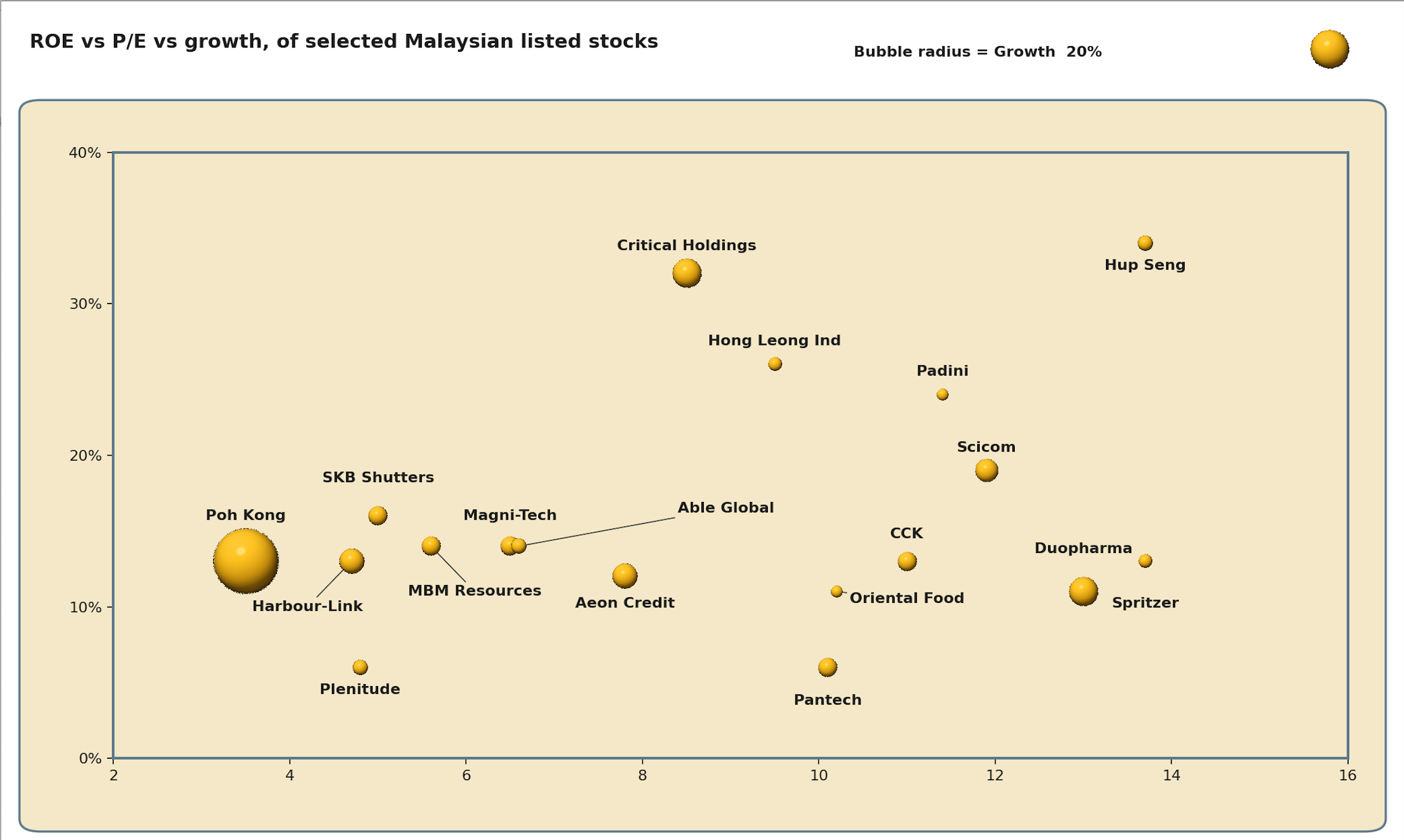

There are around 1000 stocks listed on Bursa Malaysia, so I thought there’s got to be more interesting stuff. Unlike smaller exchanges, can’t do A-Z, so I used substacker Floebertus bubble chart screening method for small caps using ROE, P/E and growth (and a few more steps, see link), calibrated to Poland, but applied to Malaysia. Got this result:

CCK, Critical Holdings

So it found CCK and Critical Holdings which are solid companies that I have already written about. Annoyingly, Critical Holdings which I was very close to buying just keeps going up (from 0.58 to 0.72 now). My watchlist might be outperforming my portfolio - but both are doing good. What’s the implication of that? That the screening and first impressions of A-Z look throughs are good, but everything else is a waste of time. I’ll put that thought aside and keep going!

Poh Kong (Market Cap 116M USD)

Poh Kong is a stand out here, so I had to check what’s going on. It is one of the largest jewellery retailers in Malaysia, and also a gold bullion retailer and trader - customers come in and buy gold bars, gold coins, and gold investment products in addition to jewellery. So Poh Kong holds a lot of gold as inventory, and the increase in gold price in 2025 pushed up earnings by a revaluation of inventory, increased margins, and caused more people to be interested in buying gold. If gold price was to go down, all these things could go into reverse, so the company is to some extent a leveraged bet on gold. The current situation with high gold price amid the Iran war and global uncertainty is about as favourable an environment as Poh Kong has ever seen.

Still, Poh Kong is a real, durable business with genuine franchise value - 100 outlets, recognised brand, loyal customer base, genuine manufacturing capability. In a normalised situation with flat gold price and no gold buying frenzy, margins go back to maybe 5%, revenue down 35%, profit halves. Even in this scenario, it would actually still be quite cheap (P/E around 7), but Im passing as the idea is to invest in the Malaysian economy, not bet on gold.

Plenitude (Market Cap 147M USD / 580M MYR)

This company has been covered extensively since 2024 by the author of Envision Malaysia 10x, a Malaysia-focused Substack well worth reading.

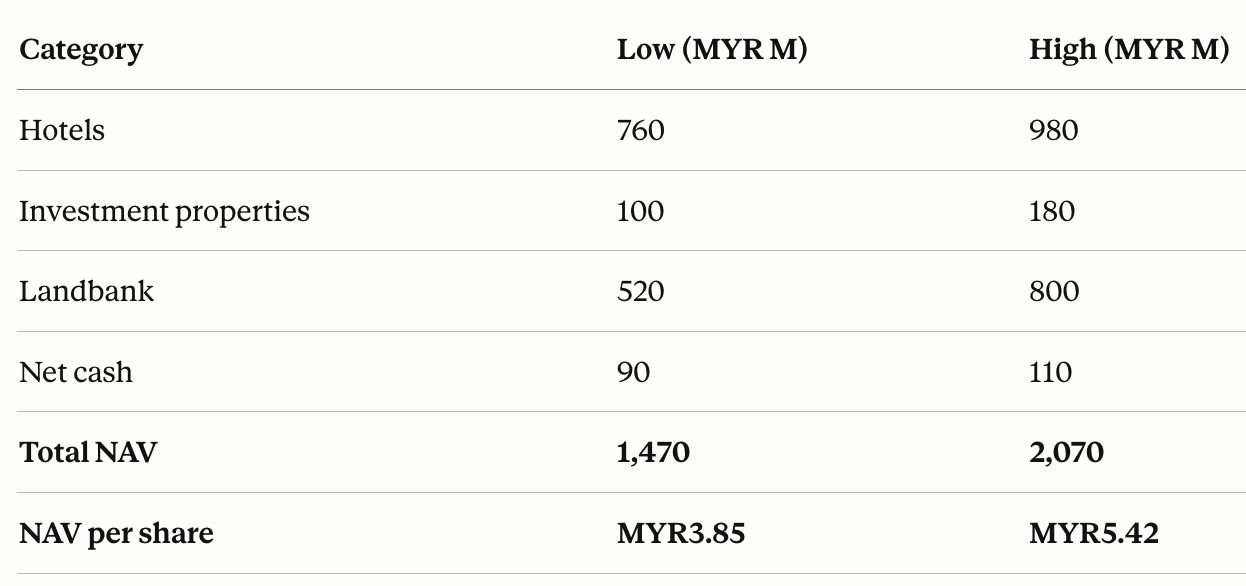

Plenitude is a property developer and hotel owner with a landbank worth more than its market cap, a substantial cash pile, a recovering hotel portfolio across Malaysia and Asia, and a long history of chronically under-earning its assets - now showing signs of operational recovery at a price that still barely reflects its balance sheet, let alone its earnings power.

Estimated market values are as follows:

And the current stock price is 1.55, which is 0.4 of the low NAV estimate. Now Malaysian (and other) property developers typically have a structural discount to NAV at 0.4 to 0.8 or so.

Plenitude is not a pure developer though, they also own hotels in Malaysia, South Korea and Japan. The hotels hypothetically spun off as a separate REIT mandated to distribute 90% of income, could be priced at close to NAV. As it stands the market has no clean (or non-lazy) way to price the hotel portfolio separately, so it applies the developer's discount to the whole thing.

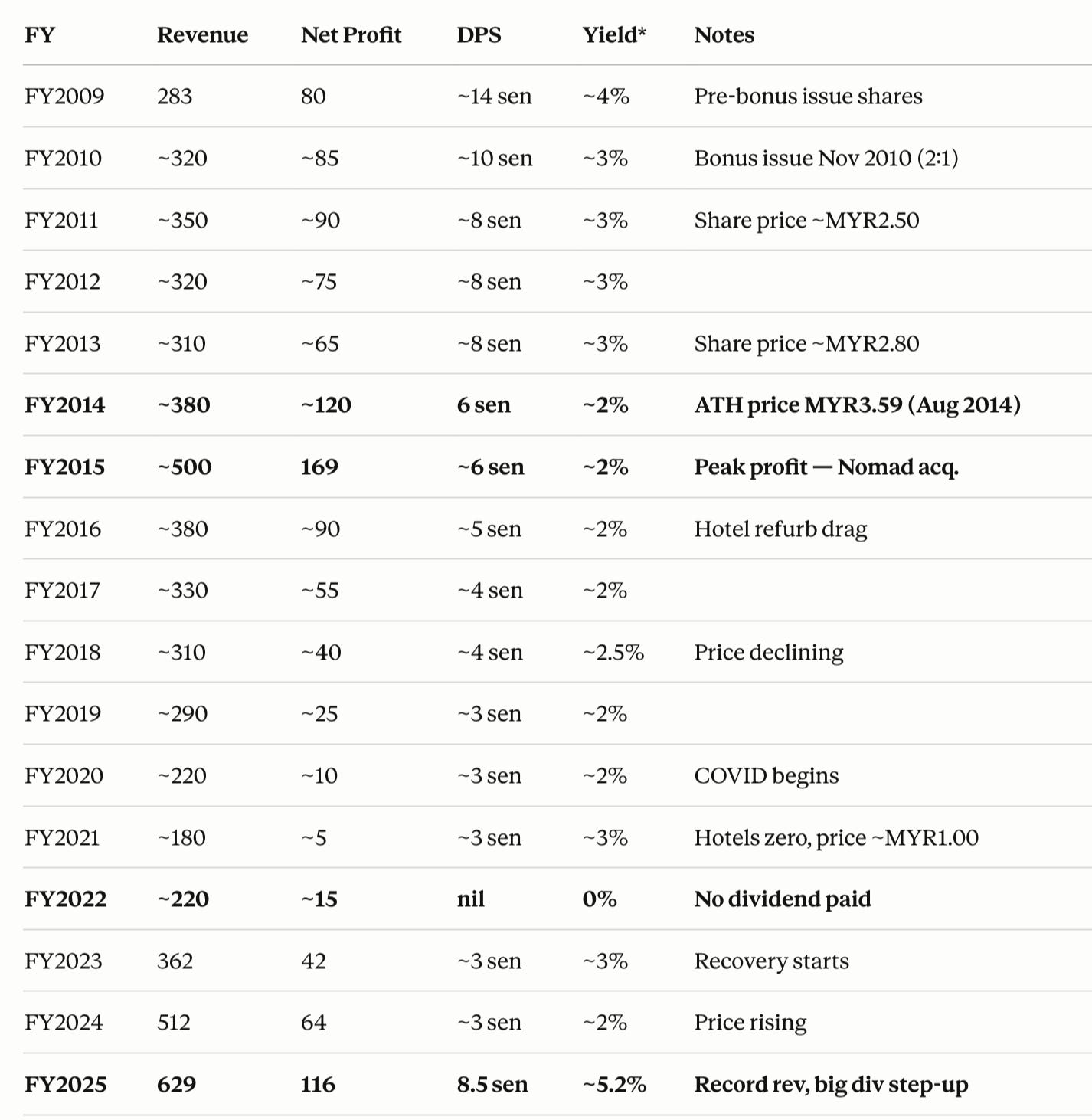

Historical revenue, earnings and dividend yield are as follows:

Here one can see the ups and downs of the property cycle, and also the first clues as to why Plenitude is so cheap.

From 2010 to 2022, Plenitude took the cash generated by an excellent property development business and poured it into a hospitality portfolio that delivered returns far below the cost of capital. This is capital destruction in slow motion.

The numbers tell the story brutally. In FY2010-2011, the property business alone was generating MYR 85 - 90M net profit on a relatively lean asset base - ROE of approximately 12%. By FY2021, the entire group with twice the assets was generating MYR 5M net profit - ROE of under 1%. And even before Covid ROE was low.

What happened in between was a series of hotel acquisitions and refurbishments that consumed enormous capital:

Ascott Gurney Penang (2015, Gurney Resort acquisition) - 259 suites, sat under refurbishment until March 2022. Seven years earning nothing.

Acquisition of a whole company (Nomad) owning 4 hotels in Malaysia (2015) near peak cycle, paid for in new shares at MYR 2.50 per share, tripling the share count. Diluted existing shareholders dramatically.

Travelodge Ipoh (2018), Travelodge Seoul (2019), Travelodge Osaka (2022) — successive capital deployments into a sector that was already underperforming.

The 200M+ MYR refurbishment programme across the portfolio, which consumed cash for years before generating any return.

Hotels in prime locations do compound in value over time, and the portfolio today - with Ascott Gurney Penang, Novotel KL, Mercure Penang Beach all operating at post-refurbishment levels is materially better than what was acquired in 2015. But the whole process of dilution, years of lost returns, has dented shareholder confidence.

Now with the hotels ready and operating fully, and the property cycle in Malaysia turning up in the geographies where Plenitude is most exposed, earnings are quite likely to at least stay high and possibly accelerate. The question is just if management stops doing value destroying hotel acquisitions, and instead starts doing more sensible capital allocation like returning funds to shareholders. Management has been mostly silent on the issue, but at least the increase in dividend 2025 was a good sign.

I’m so far coming to a similar conclusion as Mr A on this one, that it’s a big upside and limited downside. Or as Monish Pabrai calls it heads I win, tails, I don’t lose much.

The asset value is a floor, plus that the trailing P/E is just 5. It looks like plenty of earnings will be coming in, but what will management do with them?

The People behind Plenitude

Looking at ownership, one more issue comes up. One of the most powerful figures in Malaysian political and business history Tun Daim who passed away in 2024 held (with his family) a controlling stake (32%) in Plenitude via a company called Ikatanbina. Daim served as Finance Minister twice under Mahathir Mohamad (1984–1991 and 1999–2001), and built an enormous private business empire across banking, property, media and infrastructure.

Daim operated via proxies, and it is not entirely clear how much he and his family owned and still own. The second largest shareholder (22%) Fields Equity may or may not be connected to the Daim family.

There is little public record of the founding of Plenitude. What is known is that Plenitude was incorporated in November 2000, just before Daim completed his second tenure as Finance Minister (he left in May 2001). The timing is consistent with a deliberate structure - creating a property vehicle while still in government would have been problematic, but doing it at the very end of his tenure or immediately after fits the pattern of how politically connected Malaysian businessmen have historically parked assets. Daim's family held control through Ikatanbina from the outset, with Chua Elsie - apparently a trusted operator within his network - installed as Executive Chairman to run the business.

Madam Chua Elsie ran the business throughout all these years, but has minimal ownership, and is still there but as Non-Executive Chairman. She has generally a good track record for property development and visible cost discipline, but is also responsible for the hotel investments.

Essentially, this is not a founder-operator business in the classic sense - it is a politically connected family's property arm given operational management by a trusted executive, which explains both the access to prime land and hospitality assets over the years, and the opacity that has characterised its ownership and governance throughout its history. Not unusual for a frontier market, but I do prefer classic founder led businesses.

Daim and his wife were charged in January 2024 with failing to declare 71 assets as part of an anti-corruption probe. Daim died before the case concluded and charges were dropped, but his wife Na'imah faces separate charges and investigations continue across the family's asset holdings.

So we have directors and management with no meaningful ownership stake, and an owning family in legal trouble. There is a problem of alignment here, a risk of forced selling, but also a chance of a new competent owner coming in.

.

In the context of African banks I previously mentioned the risk of mangement siphoning off funds to themselves. I recently stumbled across an interview with investor Michael McGaughy who has written very clearly and funnily about exactly this, calling it Big Tycoon risk.

What about Big Tycoon risk for Plenitude?

McGaughy talks about the structure of and around a company that creates incentives and possibilities for a Big Tycoon to move funds from the company to a vehicle the Tycoon or his family controls to a 100%.

Related-party transactions

This is the core Big Tycoon concern. Looking at what’s publicly observable: Plenitude’s annual reports don’t disclose significant related-party transactions with Ikatanbina or Daim-family entities. The company’s business is reasonably self-contained - it develops its own land, runs its own hotels under Travelodge/Ascott/Mercure brand licensing (not family-controlled brands), and manages through external hospitality operators where needed. The hotel acquisition strategy at low 6-6.5% IRRs is a point of concern, but there’s no obvious vertical integration with family-owned suppliers, no known unusual procurement arrangements, no visible asset transfers at questionable valuations.

The land bank was acquired in 2000-2004 at prices that have appreciated 30-60x. If the family were extractive, you would expect them to find ways to monetise this appreciation through related-party transactions - selling parcels to Ikatanbina-linked buyers at below-market prices, for instance, or using family entities as intermediaries in development projects. The fact that the land bank has been held on balance sheet at historical cost for 20+ years, rather than being quietly dismembered through related-party sales, is strong evidence against active Big Tycoon extraction.

Has the controlling shareholder kept minorities starved of returns?

A Big Tycoon who wants cash for himself would typically see dividends as giving away his money to other people. Plenitude has had dividend yields around 2% with a 10-25% payout ratio is low by property developer standards, which is a yellow flag in McGaughy’s framework. Plenitude’s pattern - modest dividends, large retained cash buffer, ongoing reinvestment - is more consistent with conservative management reinvesting for growth than with extractive control. The 300M MYR cash buffer held consistently since 2010 actually argues against the Big Tycoon pattern, because an extractive controlling shareholder would typically find ways to get that cash out rather than letting it sit.

Are Management incentives aligned with the Tycoon, but not with minority owners?

In a pure Big Tycoon framework the low management ownership would be alarming because it suggests management serves the controlling shareholder rather than the broader shareholder base. But in Plenitude's specific case, a different reading is plausible: Chua Elsie has been at the company since 2002, was Executive Chairman through the entire listed period until 2018, took her salary to 24,000 MYR during COVID when non-executive directors earned more, and runs the company on observable frugality (two-person sales offices, lottery-draw launches to avoid agent commissions, Travelodge brand licensing to reduce reinvestment). These are not the signals of a rent-seeking manager enriching herself at shareholders' expense. They're the signals of someone who identifies with the enterprise and runs it austerely.

Big Tycoon is gone, what now?

There is no second-generation Daim family representative visible in Plenitude's operational structure. This is actually interesting - if the family considered Plenitude a core strategic asset, you'd typically expect to see a child or nephew on the board or in senior management. Their absence suggests Plenitude has been treated as a passive financial holding rather than a core family business. This reduces Big Tycoon risk in one direction (less active family involvement means less active extraction) but increases it in two other ways:

if the family needs cash for legal defence, they may reach for the one passive asset they haven't been extracting from. But maybe the family is too weakened and under too much legal scrutiny to do this.

with limited owner oversight, the senior management could start jacking up their salaries, and doing Big Tycoon stuff themselves. However, looking at Chue Elsie’s leadership style, it does not seem this would fly.

Conclusion

Well, one gets way more real estate for the money with Plenitude than with Matrix Concepts. Upside is indeed big, but if Management is unaligned and siphons off funds, it is still not a good investment. I don’t think that’s the case though, and I’m tempted switching over a part of the Matrix investment to Plenitude. Super-interesting to follow what happens to Plenitude anyway.

I love seeing a Floebertus chart

Thanks, I am really enjoying your Malaysian series. It's really amazing how many property developers they have in Malaysia, there are everywhere. Not my favourite type of business, but it's true that they're really cheap over there...